What’s your bank’s mobile strategy?

Not if, not when, but how

- |

- Written by Chris Cox, First Data & David Albertazzi, Aite Group

Banks continue to take advantage of mobile banking and payment solutions for omnichannel customers as they live more connected lives. Mobile banking, in particular, continues to make strides toward becoming the key channel. Customers expect banks to deliver user-friendly, feature-rich technology. However, banks must also provide efficient transactions, relevant communications, and, above all, security.

Understanding consumers’ increasingly complex path to purchase, including which channels they use to engage, explore, and buy, has become a journey for many retailers and financial institutions. In 2014, the goal no longer is facilitating an effective multichannel experience. Now the industry is chasing the omnichannel experience—consumers are always engaged in a continual shopping and selling experience that transcends communications channels and locations.

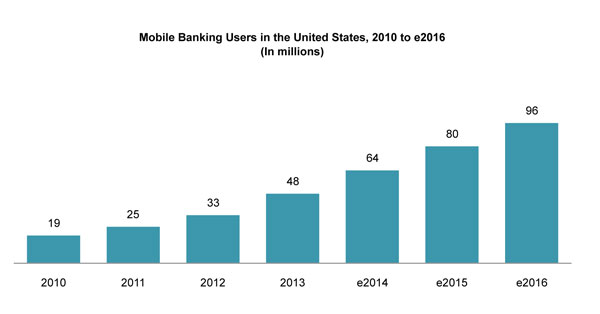

After years of development and enhancements, mobile banking is quickly becoming a “must have” for banks of all sizes, and adoption of mobile banking continues to grow. There are about 48 million mobile banking users currently in the U.S., and Aite Group forecasts that number to nearly double by the end of 2016.

For a larger version, click on the image.

For a larger version, click on the image.

Widespread research shows that the lack of mobile banking offerings is increasingly becoming a dominant factor for consumers switching banks. Consumers will increasingly look for a mobile solution that goes beyond basic banking functions to enable their overall commerce experience: efficiently select the right financial product, manage money, and make payments. Therefore, a personalized mobile solution should be top of mind for banks today in attracting and retaining customers.

In order to ensure efficiency, relevancy, and security, banks should first focus on specific issues that can be addressed in a mobile context, such as a better customer experience or better internal operations when it comes to governance and risk reduction. They can then determine how to address those issues with an open and scalable infrastructure. Integrated applications can deliver a seamless experience across channels as well as valuable data that helps drive new levels of targeting, personalization, and measurement.

Keeping security top of mind

Security remains a significant concern for banks. They need a comprehensive mobile solution that allows them to meet compliance requirements, reduce risk, and securely process in-store and online transactions. Combining data sources, cutting-edge analytics, and customer management helps to effectively assess and manage credit risk and streamline the overall strategy.

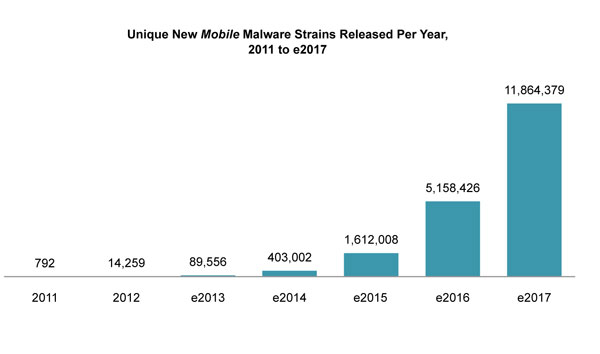

While the number of malware threats in the mobile environment remains much smaller than those online, this platform is by no means immune to threats. The mobile malware population is growing at a much faster rate than the online threat. The number of new strains of malware deployed—only 792 in 2011—jumped nearly twentyfold in 2012. At the current pace, it will nearly surpass 400,000 unique strains of malware deployed in 2014. Trojans designed to steal data and compromise banking credentials represent the bulk of the new malware developments.

For a larger version, click on the image.

For a larger version, click on the image.

Security features must continuously be maintained and expanded to ensure that the mobile channel remains trusted by customers. The strategy that many financial institutions undertake is to augment their security infrastructure with complementary layers of technology that make it harder for fraudsters to penetrate the defenses. However, the threat environment is moving very fast. Therefore, banks’ approach to security needs to encompass multiple solutions, both native to their platforms and outsourced to specific point-solution providers.

Because banks are expected to serve as trusted and reliable advisors, they can reduce customer security concerns by introducing and facilitating new types of authentication that go beyond mere compliance.

As mobile banking solutions extend into payments, the combination of end-to-end encryption (E2EE) and data tokenization provides enhanced security by protecting sensitive cardholder data from the point of capture through delivery to the payment processor. Banks can also utilize password protection and fingerprint or voice recognition, as well as send relevant notifications on irregular customer activity such as large withdrawals or suspicious transactions.

Bank examiners advocate an optimized mix of layered technologies that strike the right balance between security and user experience, but this is no easy task. Tools include: device fingerprinting, behavioral analytics, malware detection, knowledge-based authentication, one-time password tokens, out-of-band authentication, transaction monitoring, transaction signing, endpoint protection, and biometrics.

Looking ahead

As omnichannel technology enables consumers to bridge their online, mobile, and offline worlds, they are empowered to know more, do more, and share more. These capabilities are driving higher expectations of banks. Understanding the transition in consumer thinking is quickly becoming a requirement for banks to create closer customer relationships and keeping those customers secure.

In light of the escalating threat environment, capped with the 2013 breach of Target that compromised 70 million card numbers along with other personally identifiable information, there is an increasing push in 2014 to encrypt and tokenize sensitive data. Card associations and banks are continuing to focus card tokenization schemes to address payment card data security in brick and mortar, online, and mobile context.

This is also a critical data security step for merchants. Just as banks build their online and mobile application security with the assumption that the endpoint is already compromised, the approach to merchant data security needs to assume the eventual compromise of the merchant's systems.

Beyond the need for security, consumers today seek personalized and expedient omnichannel experiences, which can be achieved by utilizing technologies like Bluetooth low energy beacons, tokenization, and card-linked offers. Banking expectations are no different. While speed and efficiency are important, thoughtful strategy is the key driver in the success of FI mobile initiatives.

In order to stay competitive amidst the mobile evolution, banks must offer convenient options and demonstrate innovative security solutions that help them effectively manage risk and fraud. Successful mobile payment solutions will be those that go beyond simple card swipe replacement to solving real consumer problems in unique and innovative ways.

As mobile capabilities mature and branch traffic declines, many banks are rethinking their branch network. While many may focus on reducing costs, some financial institutions look to transform their branch network into centers for sales and guidance where relationships will be built and where consumers can complete personalized banking services that they started online or on their mobile device.

Retailers and bankers have opportunities to harness their digital capabilities and infuse them into their physical locations. Brands that respond to these trends will be better positioned to drive incremental sales, build customer loyalty, and provide an outstanding customer experience.

Tagged under Lines of Business, Technology, Payments, Mobile,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- How Banks Can Unlock Their Full Potential

- Banking Exchange Interview: Soups Ranjan Founder and CEO of Sardine Discusses AI

- Digital Wallets Account for Half of Online Sales

- Unlocking Digital Excellence: Lessons for Banking from eCommerce Titans