Eye on 2016 deposit trends

SNL Report: Low-cost deposits the norm for now, but new story in '16?

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Kevin Dobbs and Zuhaib Gull, SNL Financial staff writers

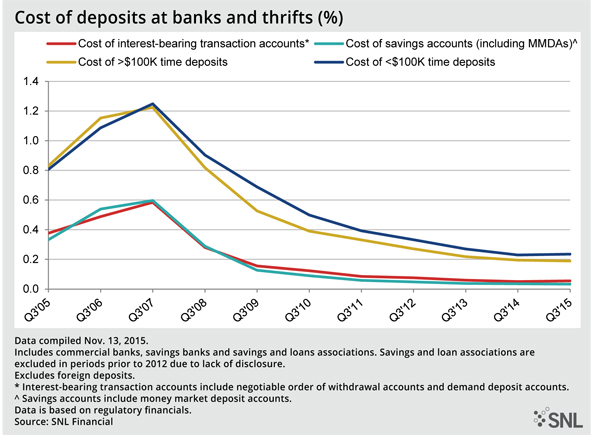

Low-cost deposits came easy for U.S. banks and thrifts in the third quarter of 2015, continuing a multiyear trend that has coincided with the protracted low interest rate environment.

The cost of money market demand and other savings accounts hovered near zero in the quarter ended Sept. 30, according to an SNL Financial analysis of regulatory data, and funding costs overall hung around historic lows.

Deposit costs started moving down in 2008 and have remained low ever since. With many Americans taking conservative stances with their money and often deciding to park it in savings accounts despite the low rates, most banks have had little trouble amassing deposits at relatively little expense.

Looking at some banks’ experiences

Wells Fargo & Co.'s experience is a case in point. The bank, spread across most of the country, has generated strong deposit growth for several years, even as the cost of gathering such deposits declined, CFO John Shrewsberry said at a November conference.

Wells grew average deposits by more than $70 million in the third quarter alone, to about $1.2 trillion. Shrewsberry said Wells' third-quarter deposit cost was 8 basis points, down 2 basis points from a year earlier. Through the first nine months of 2015, he said, the bank grew deposits by 8%.

But mounting expectations for change on rates as soon as December has bankers and analysts looking ahead to an evolving playing field in 2016.

As Bank of Hawaii Corp. Chairman, President and CEO Peter Ho put it to SNL, nobody knows for sure when the rate environment will shift, but most banks are wisely braced for change in the year ahead and are mindful that depositors' willingness to move their money around likely will increase when rates rise.

"Rates will go up at some point," Ho said. "We do know that much. And things [will] start to change when that happens."

All eyes remain glued to the Fed

The Federal Reserve has kept short-term rates low since the 2008 financial crisis. But Fed policymakers, including Chairwoman Janet Yellen, have made it known that the first rate hike in years is on the table when officials meet in December. A particularly strong October jobs reports—employers grew nonfarm payrolls by 271,000 jobs—furthered the prospects for a rate increase by the Federal Open Market Committee, the Fed's policy arm.

"Expectations for a rate hike at the December FOMC meeting have picked up in recent weeks," Matthew Kelley, a Piper Jaffray analyst, said in a November report. He noted that intermediate and longer-term U.S. Treasury rates have moved up, indicating market expectations for a rate bump.

Fed officials have said that when they do start to move on rates they likely would begin with a modest 25 basis-point increase and then gradually build up to normalized levels from there. Such developments could lead to higher funding costs by the second half of 2016.

Return of rate wars?

If banks respond to a shift in Fed policy by paying up for deposits, observers say, it could mark the beginning of a new era of more heated competition for funding. If they are able to fetch higher rates, many depositors likely would move their money out of MMDAs and into less flexible but higher-paying accounts. And as they make these moves, they are likely to shop around for the best rates.

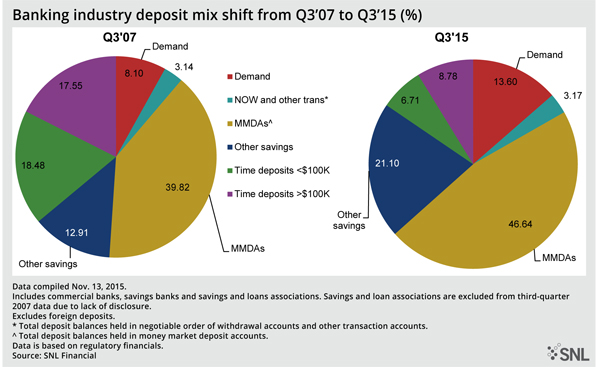

MMDAs accounted for 46.64% of U.S. deposits in the third quarter, up from 39.82% in the third quarter of 2007, prior to the Fed's response to the financial crisis, according to the SNL analysis.

But most banks are currently well-stocked on funding and could afford to allow some deposits to run off. As such, observers say, many banks are likely to move gradually on raising rates for depositors while moving more swiftly to boost rates on loans in order to enjoy the benefits of higher rates.

Banks' net interest margins—a key measure of lending profitability—have been under pressure for years amid the low-rate era. When rates rise, margins could expand and bolster bottom lines.

That noted, growth-minded banks that are eager to expand lending in coming years have been working hard to gather core deposits—local checking and other accounts that tend to cost banks less and that customers are less likely to move from one bank to another because of the hassle involved.

Community banks, in particular, have eyed such deposits as they have pursued acquisition targets, Jefferson Harralson, an analyst at Keefe Bruyette & Woods Inc., told SNL. "That shows you their importance," he said.

Stuart, Fla.-based Seacoast Banking Corp. of Florida, for example, recently highlighted the core deposits that it stands to pick up with its planned acquisition of Floridian Financial Group Inc., the Lake Mary, Fla.-based parent of Floridian Bank. The target has $361 million in deposits, about 86% of which are low-cost core deposits.

After announcing the deal earlier this month, Seacoast executives said those core deposits are important as the bank looks to fund increased lending and expand alongside the growing economies and population bases of markets such as Orlando and other cities in Florida.

Harralson said after that deal was announced that he expects the pursuit of low-cost deposits to play a role in ongoing merger-and-acquisition activity — now, as banks prepare for a change in rates, and later, when the environment actually does begin to shift.

This article originally appeared on SNL Financial’s website under the title, "Low-cost deposits the norm for now, but new story in '16?"

Tagged under ALCO, Management, Financial Trends, Risk Management, Rate Risk,