Minnesota heads for “show” in 2014 M&A

SNL Report: State is #3 in M&A deal volume

- |

- Written by SNL Financial

By Jack Chen and Kevin Dobbs, SNL Financial staff writers

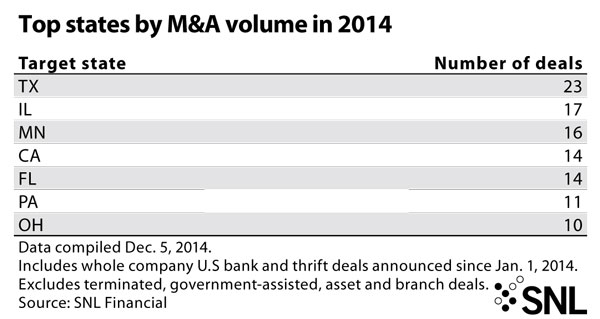

Minnesota ranks third among all states so far in 2014 in bank merger-and-acquisition activity, as rural and out-of-state buyers look to move into the economically diverse Twin Cities of Minneapolis and St. Paul.

As of Dec. 5, buyers had announced 16 whole-bank deals involving Minnesota targets in 2014. Only more populous Texas, with 23 deals, and Illinois, with 17, outrank Minnesota in terms of deal volume this year, according to an SNL Financial analysis.

Rural banks hunger for metro diversification

Most recently, in early December, Greenbush, Minn.-based Border Bancshares Inc., the holding company for Border State Bank ($369.5 million), said it had inked a deal to buy from First Advantage Bancshares Inc. its Coon Rapids, Minn.-based First Advantage Bank ($70.2 million). The deal involves the buyer, a founding shareholder of the target bank, acquiring the stock and expanding its investment in First Advantage, which operates in the northern suburbs of Minneapolis.

Border Bancshares Chairman, President and CEO Robert Hager told SNL that he views the acquisition as "good diversification" for his company, which, at its northern Minnesota base, is focused in large part on agriculture and rural lending. Making its ties to the Twin Cities formal via the deal gives the company a broader array of customers from whom it can draw deposits and generate lending business, he said.

The Twin Cities metro area, with more than 3 million people—more than half the population of the entire state of Minnesota, known as the land of 10,000 lakes—is the "center for commerce and government and everything in Minnesota," Hager said. That includes banking industry talent, he said.

Rural banks, while benefiting from a strong agriculture sector, want to diversify now while they are on solid footing so that they can capitalize on other industries in the future when the farm sector, inevitably, will slow.

And, as farm operations grow now, they consolidate in the hands of fewer farm families—bigger farms, but fewer owners and operators— so small-town Minnesotans increasingly move to or near the Twin Cities for college and jobs. Banks outside the metro want to build pipelines to the younger talent that is blossoming in Minneapolis-St. Paul, Hager and others say.

Community banks making their moves

At the same time, Hager said, community banks within and outside of the metro area face the same challenges as their peers do across the country: heavy regulatory pressure and high compliance costs; low interest rates that have crimped margins; and intense competition from larger lenders, including regional heavyweights based in the Twin Cities area such as U.S. Bancorp and TCF Financial Corp. More community banks, tired of grappling with such burdens with small asset-bases, are deciding either to become sellers or buyers.

Either way, the idea is to gain heft to boost lending limits and broaden product offerings in order to better compete, and to create larger bases over which to spread out and better absorb compliance costs.

"The economics of the banking business have changed," Hager said, making it increasingly difficult for many small banks, particularly those under roughly $100 million in assets, to produce the returns necessary to satisfy shareholders. "That's going to heighten [M&A] activity."

Among those under that $100 million threshold is First Advantage, Hager and company's target.

James Amundson, president and CEO of First Advantage, told SNL that his bank decided to sell because management and the board realized that it simply needed greater size and more expansive offerings of products and services to compete with bigger lenders and to navigate the other headwinds.

"That's what drove it for us," he said. "And I think you'll see that with a lot of our peers."

Both Amundson and Hager said they anticipate that the M&A wave in Minnesota will continue to build and extend into 2015. They both noted that Minnesota has a relatively high number of small, privately held banks, and many lenders could sell to gain size and access to public markets.

Digging into the numbers

SNL data show there are 340 commercial and savings banks in Minnesota; on a per capita basis, it ranks sixth among all states in terms of the number of banks chartered in the state. What's more, among the banks in Minnesota, more than half are privately held and under $100 million in assets, according to an SNL analysis.

Of the 16 deals announced to date in Minnesota this year, nine involved targets under $100 million in assets.

For a larger version, click on the image.

For a larger version, click on the image.

At the same time, Hager said, community banks within and outside of the metro area face the same challenges as their peers do across the country: heavy regulatory pressure and high compliance costs; low interest rates that have crimped margins; and intense competition from larger lenders, including regional heavyweights based in the Twin Cities area such as U.S. Bancorp and TCF Financial Corp. More community banks, tired of grappling with such burdens with small asset-bases, are deciding either to become sellers or buyers.

Either way, the idea is to gain heft to boost lending limits and broaden product offerings in order to better compete, and to create larger bases over which to spread out and better absorb compliance costs.

"The economics of the banking business have changed," Hager said, making it increasingly difficult for many small banks, particularly those under roughly $100 million in assets, to produce the returns necessary to satisfy shareholders. "That's going to heighten [M&A] activity."

Among those under that $100 million threshold is First Advantage.

James Amundson, president and CEO of First Advantage, told SNL that his bank decided to sell because management and the board realized that it simply needed greater size and more expansive offerings of products and services to compete with bigger lenders and to navigate the other headwinds.

"That's what drove it for us," he said. "And I think you'll see that with a lot of our peers."

Both Amundson and Hager said they anticipate that the M&A wave in Minnesota will continue to build and extend into 2015. They both noted that Minnesota has a relatively high number of small, privately held banks, and many lenders could sell to gain size and access to public markets.

SNL data show there are 340 commercial and savings banks in Minnesota; on a per capita basis, it ranks sixth among all states in terms of the number of banks chartered in the state. What's more, among the banks in Minnesota, more than half are privately held and under $100 million in assets, according to an SNL analysis.

Of the 16 deals announced to date in Minnesota this year, nine involved targets under $100 million in assets.

Chris Vanderpool contributed to this article.