“Big flip” coming in deposit costs?

Factors point to return of dominance of interest-bearing deposits—in a rising rate environment

- |

- Written by Neil Stanley, The CorePoint & TS Banking Group

Domestic deposit interest expense increased by 42% from 2016 to 2017. With the Fed’s latest rate-setting meeting earlier this week confirming its continued path towards higher rates, banks must adopt strategies to meet a major change of conditions.

Domestic deposit interest expense increased by 42% from 2016 to 2017. With the Fed’s latest rate-setting meeting earlier this week confirming its continued path towards higher rates, banks must adopt strategies to meet a major change of conditions.

The composition of banking industry funding has changed dramatically over the past 30 years. How will the dynamics of industry growth, digital technology, and interest rate changes impact bank financial performance?

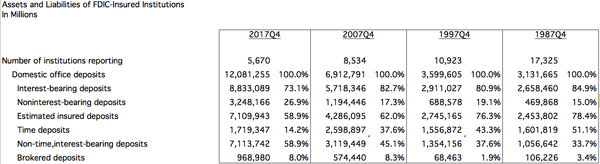

In the FDIC data below, notice the increase in non-interest-bearing deposits in the last ten years after decreasing in the prior decade. What will be the impact of rising interest rates and new technologies? Will recent trends continue or will the variables that created these trends be modified and take the industry in a different direction?

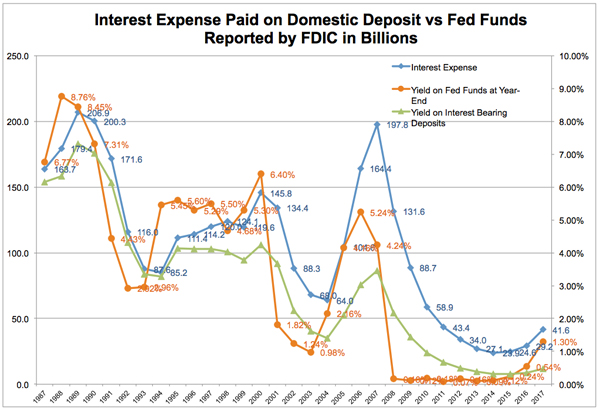

FDIC publishes a report of industry interest expense that is graphed below along with the FDIC report for savings banks and overnight fed funds at the end of the year

How environment is changing

To model the industry’s future balance sheets and income statements, we must recognize the capacity and propensity of depositors to consider their options and redirect their deposit funds. We need to factor in today’s ubiquitous access to banking information and the depositors’ ability to transfer funds that has become widespread in this digital environment.

Depositors have vastly more viable options today, including online-only banks. Today they need only exert minimal effort to access their choice of deposit options. It is easily conceivable that a greater percentage of deposits will seek a market rate of interest as the incentives increase with every hike in interest rates. We project that the percentage of interest-bearing deposits to total deposits will rebound back to the trajectory that was observed prior to the Great Recession.

Another factor that will likely impact this ratio is the 2011 repeal of Regulation Q—mandated by the Dodd-Frank Act— which effectively allowed the payment of interest on business checking accounts.

While the setting of interest rates on business deposits relative to Fed funds may not be as aggressive as for retail deposits, it seems clear that this will contribute to a higher percentage of deposits that will be interest bearing for banks than prior to 2011, ultimately producing greater deposit interest expense for banks.

How conditions may change

We anticipate that banks will compete successfully with other investment alternatives in order to grow domestic deposits at levels to keep pace with loan demand.

As the economy expands, interest rates will continue toward historically normal levels. Over the past 30 years, the average Fed funds rate has been over 3%, even with the unprecedented low rates of the past ten years. We consider any Fed funds rate below 3% to be easily supported for projection purposes.

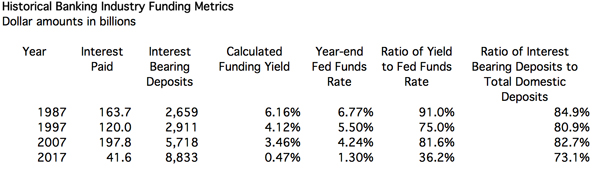

Given these expectations we assess the historical “ratio of yield to Fed funds rate” and the “ratio of interest-bearing deposits to total domestic deposits.” Here is a summary of the primary parameters of historical domestic deposit funding cost.

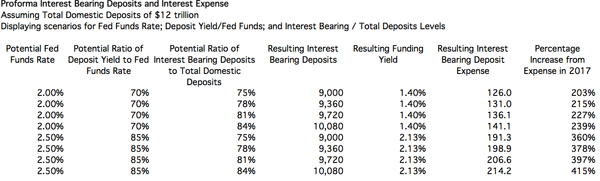

From these results we seek to create realistic scenarios for Fed funds rates; ratio of yield to Fed funds; and ratio of interest-bearing deposits to total deposits to estimate the expected change in industry interest expense for domestic deposits.

As interest rates on overnight fed funds rise to 2.00%–2.50%—the March 21 decision pushed it to 1.5%-1.75%—we can expect the yield of interest-bearing deposits relative to Fed fund yields to return to historical rates and beyond. Please consider that the industry has fewer time deposits than in previous rising-rate environments. Those would naturally lag rising rates.

We display 70%-85% in the scenarios below. Lastly, we expect the ratio of interest-bearing to total domestic deposits to adjust to levels between 75%-84%.

As this happens we can project the increase in bank interest expense to increase from 2017 levels by roughly 200%-415% with annual interest expense levels projected between $126 billion and $214 billion.

This will be an unprecedented increase in bank expense from the 2017 level of $41.6 billion.

This escalating expense could create significant stress on many bank income statements and management teams.

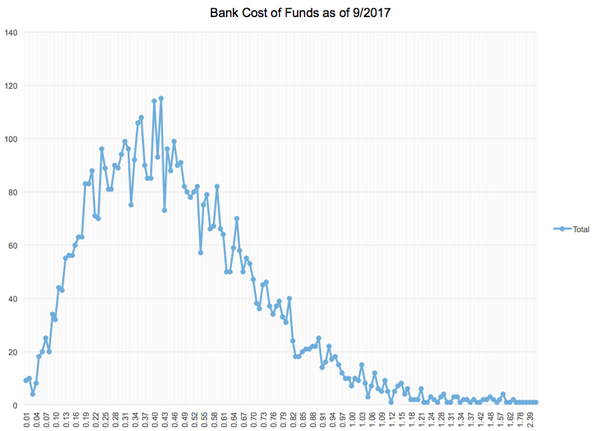

Note that funding cost is not homogenous across the industry. The cost of funds as of September 2017 ranged from 1 basis point to over 200 basis points for a handful of banks; but the median reported was 43 basis points. Further analysis reveals that 10% of banks had costs of funds below 0.18%, and 10% of banks had cost of funds above 0.80%. Thus this range of 62 basis points in cost of funds covered 80% of the banks in the middle.

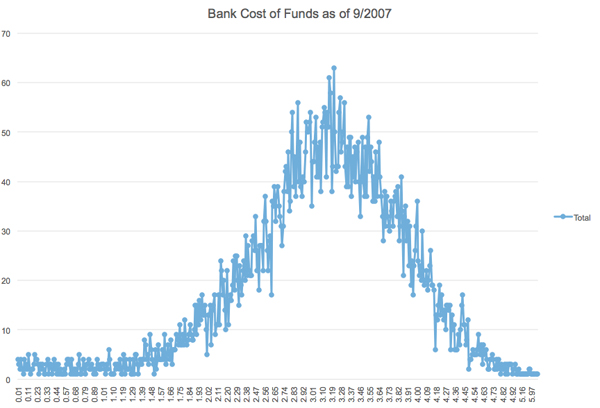

Going back to 2007 data gives us insight about the dispersion of results that we might expect from the development and execution of different funding strategies as rates rise. Here is the same graphic presentation of the dispersion of cost of funds from a decade ago.

The comparable statistics in 2007 indicate that the median cost of funds was 3.15%. We find at that time 10% of banks had cost of funds below 2.09% and 10% of banks had cost of funds above 4.03%. Back then it took a range of 194 basis points to cover the spectrum of cost of funds for 80% of the banks in the middle—versus 62 basis points in 2017.

The dispersion between high-performers and low-performers was observed to be much greater in the higher interest rate environment. As interest rates dropped, banks that exceled at cost of funds did benefit, but to a lesser extent than in previous environments.

Implications for days ahead

As a result of what’s been outlined, many banks therefore have spent relatively little time and effort on deposit strategy over the last decade.

This data supports the reasoning that we can expect that as interest rates rise bankers will find it will again be quite profitable to more effectively differentiate themselves and appropriately invest in creating a competitive advantage.

Given the magnitude of funding on the balance sheet, we know that incremental improvements in cost of funds have a very sizeable impact on return on assets and return on equity. The opportunity for high-performance in this category impacting overall bank performance will become greater as the magnitude of interest expense grows.

Consistent with this analysis, we now observe bankers seriously exploring better ways to establish a competitive advantage by anticipating this environment and taking action to prepare finance, retail, marketing, and client experience to compete for long-term, properly-priced retail deposit funding.

How to revamp deposit strategies

Accordingly, bankers anticipating the changes we foresee are updating deposit funding strategies to identify and communicate:

• Enhanced awareness of and empathy for the depositor journey and experience.

• Understanding of the current deposit base and the trajectory of deposit funding compared to funding needs.

• Appreciation of competitive posture. Who are the top competitors and what are they doing with pricing? What products are they offering? How are they engaging depositors?

• Adoption of tactical shifts. Methods to keep deposit pricing relevant.

• Reconsideration of the breadth of offerings. What new deposit products and technologies do we plan to offer? How do we extend offers to get growth without excessively increasing the cost of deposits we would otherwise have if we were not seeking growth?

• Examining outreach. How we engage depositors with promotional marketing efforts? How do we contact our most valued depositors? At-risk depositors? Those with most up-side potential? Prospects for new relationships?

• Connecting to customers. How we enlighten, equip, and empower our front-line to compete for and win deposit relationships. In addition, how we train, coach, and manage deposit processes.

Successful banks will design a robust set of attractive and compelling product offerings in each category. We feature a few opportunities here…

• Non-interest bearing demand deposits: Onboarding new clients with simple-to-use switching of direct deposits and automatic payments.

• Non-term interest bearing deposits: Using debit-only interest bearing accounts such as a Companion Deposit Account to provide an attractive market rate of interest to long-term savers without excessively cannibalizing existing deposits.

• Term interest-bearing deposits: Offering Smart CDs which feature the elimination of static early withdrawal penalties that excessively punish depositors for early withdrawal.

Now’s the time to act

Proactively engaging all aspects of deposit strategy now will help to significantly constrain cost of funds as it becomes a bigger factor of return on equity in this rising-rate environment.

The processes, products, tools, and training that have been deferred for so long can now be expected to produce a disproportionately large benefit because no other category of expense will grow at the same pace as interest expense.

Deposit management can quite reasonably be expected to become the largest expense management dynamic and differentiator of performance for bankers in the next few years. Success can be found when preparation and opportunity intersect.

About the author

Neil Stanley is founder and CEO of The CorePoint, a financial technology firm providing the CoreCD® deposit sales and pricing platform. He also serves as president of community banking at TS Banking Group, which operates in Iowa, North Dakota, and Illinois.

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients