Why branches still change hands

SNL Report: Branch deals about core deposits and lending profitability—not buildings

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Kevin Dobbs and Venkatesh Iyer, SNL Financial staff writers

In an era when customers are increasingly doing more of their banking business via digital means, many banks are actively downsizing the size and number of their branches via closings and sales.

SNL Financial data showed that the U.S. banking sector finished 2015 with 92,997 branches, 1,614 fewer than a year earlier. That extended a trend that dates to 2009.

But there is more to this story.

As banks unload branches, other lenders step in and buy certain locations put on the sale block—often to pick up prized low-cost deposits in anticipation of a rising interest rate environment, as opposed to simply seeking out a physical presence in a given area.

Federal Reserve policymakers in December 2015 raised short-term rates for the first time since prior to the 2008 financial crisis, and they signaled that more hikes could follow in 2016. While policymakers left rates steady following their January meeting—its targeted federal funds rate hovers between 0.25% and 0.50%—they left additional, gradual rate increases on the table for the year ahead.

That leaves bankers anticipating a higher rate environment, and those with ambitions of strong loan growth this year and beyond say that makes inexpensive deposits all the more valuable. Banks with lower funding costs—high levels of core deposits—are often best positioned to follow Fed rate hikes with rate increases on loans that are greater than bumps they may have to make to on deposits, helping boost the profitability of lending. (Editor’s note: SNL Financial’s report here was originally filed in late January. In her Feb. 10 testimony to Congress, Fed Chairman Janet Yellen was not specific in the outreach for further increases given the state of the economy.)

"I do think a lot of bankers are gearing up for that," Jacob Thompson, a managing director of investment banking at SAMCO Capital Markets, told SNL.

Rate expectations and branch deal pricing

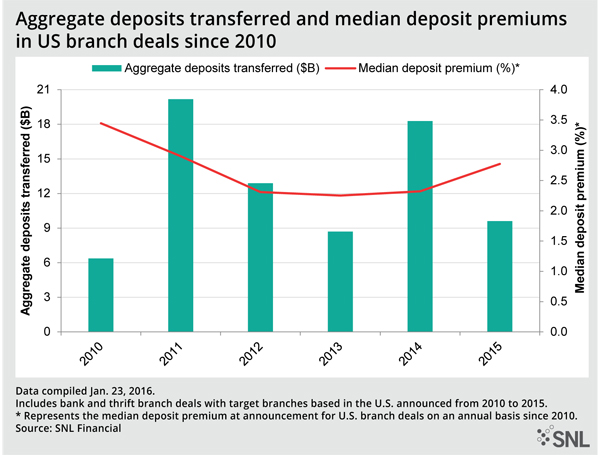

That helps explain why deposit premiums paid on branch deals climbed in 2015, Thompson said. An SNL analysis of U.S. bank and thrift branch deals found that the median deposit premium approached 3% last year, up from each of the three previous years, when the median level hung below 2.5%.

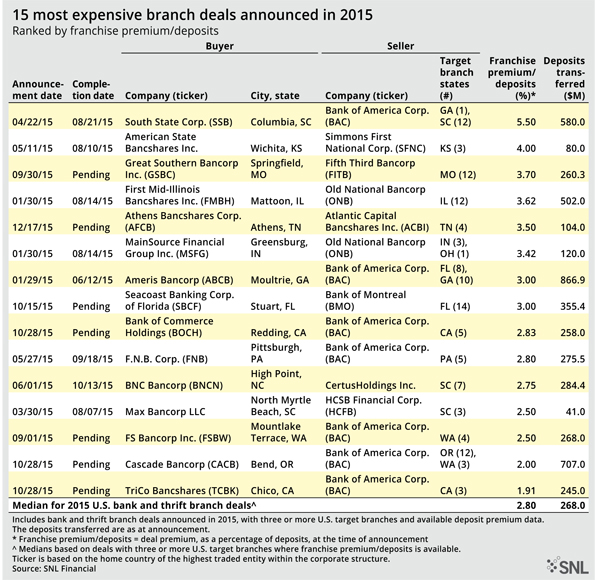

South State Corp.'s acquisition of 13 Bank of America Corp. branches in 2015 encapsulates this development. The Columbia, S.C.-based bank picked up nearly $440 million in core deposits via the deal—this was the final level following closing—and paid up to get them.

The franchise premium paid on the deposits in that deal—deal premium as a percentage of deposits at announcement—was 5.5%, the highest of all branch deals involving three or more locations last year, according to SNL data.

But South State COO and CFO John Pollok told SNL that the branches were about 40 years old and were loaded with deposits from customers who had long parked their money at those locations. "We paid a pretty high premium, but those deposits are very, very sticky," Pollok said. "We're a big believer in core deposits."

The bank also believes that it, like most of its peers, ultimately needs fewer branches. That, Pollok said, is why South State made a plan to consolidate six overlapping branches tied to the BofA deal. It was part of a broader effort to bring down branch numbers and drive in-person business to select locations where foot traffic remains high enough to make the branches profitable.

So even as it buys branches, South State looks to shutter or sell some of them off later—after it has established itself with customers at those branches and after it is comfortable it will retain the vast majority of core deposits acquired, Pollok said.

"Those core deposits, they are the main focus of our strategy," he said.

Pollok said South State has a history of steadily growing loans, so it needs to continue to bolster its low-cost funding base to both fuel that lending and maximize its profitability. That thinking gets amplified as interest rates rise, he noted, which is another reason South State was eager to seal the deal with BofA. It joined much of the industry at the time in anticipating that a shift in the rate environment was inevitable. The December rate increase proved them right.

Pollok said South State has a roughly 85% loan-to-deposit ratio. The favorable level means that, unlike competitors with lower funding bases and higher loan-to-deposit ratios, South State does not have to borrow to fund loan growth, demonstrating that its focus on core deposits gives it an advantage and helps it to compete with larger banks, Pollok said.

"Our No. 1 goal has been getting those core deposits," he said.

Click on image to enlarge.

Click on image to enlarge.

Impact on whole-bank deals

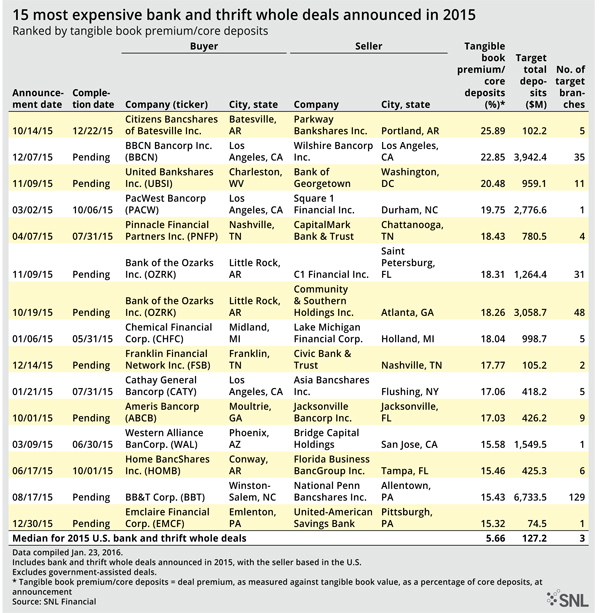

The same thinking was often applied to whole-bank acquisitions in 2015. A case in point: PacWest Bancorp's acquisition of Square 1 Financial Inc.

Assessing deals on the basis of deal premium measured against tangible book value as a percentage of core deposits at announcement, PacWest's play for Square 1 was among the most expensive acquisitions of 2015, according to SNL data. And Square 1, a venture capital-focused bank, brought only one branch to the deal table.

But it also brought a dozen loan-production offices nationally and a wealth of low-cost deposits. At the time of the deal announcement, nearly half of its $2.8 billion in deposits were noninterest bearing. So the acquisition gave Los Angeles-based PacWest both new lending opportunities and low-cost funding to help drive it, and it better positioned the buyer for an eventual shift upward in the rate environment, analysts told SNL after that deal was inked in 2015.

All of that noted, two important questions loom large: When will the Fed move to further raise rates? And how much do rates need to rise for lenders to show substantial gains in their net interest margins?

SAMCO's Thompson emphasized that any answer to the first question is merely a guess, given that Fed policymakers have said future increases are dependent on consistently solid economic data. The domestic energy sector is slumping amid low oil prices; global economic conditions are fragile; and rocky stock markets point to concerns about slowdowns in Europe and Asia infecting the U.S. [Read Yellen’s testimony here.]

But, the U.S. job market remains on solid ground, as Thompson noted, and Fed officials anticipate upward momentum in inflation. If employment levels remain strong and inflation starts to pick up, policymakers could potentially move on rates multiple times before 2016 is over.

Many bankers say that, on top of the 25 basis-point increase in rates that the Fed initiated in December, they would need to see at least two more similar hikes, perhaps three, to really show substantial benefits from higher rates. Count Bank of Hawaii Corp. Chairman, President, and CEO Peter Ho among them.

"We haven't seen much of an impact yet," Ho told SNL. "Every little bit helps, but if we can get up to a cumulative increase of 100 [basis points], that's when we'd see meaningful impact."

Click on image to enlarge.

Click on image to enlarge.

This article originally appeared on SNL Financial’s website under the title,"Branch deals about core deposits and lending profitability—not buildings"

Tagged under Mergers Acquisitions; Tokenization; Risk Management; Channels; Rate Risk; M&A; Feature; Feature3;

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients