Do’s and Don’ts when selling financial services

Reassessing the process in light of Wells Fargo mess

- |

- Written by Mike Moebs

- |

We are wrapping up a series of commentaries by our bloggers and other experts on the Wells Fargo Bank case. In this article, two former executives of Wells Fargo Bank—“Prairie Economist” Mike Moebs and guest co-blogger Dan Kleinman discuss how to avoid Wells-type issues. Mike includes more about Kleinman at the conclusion of this article.—Steve Cocheo, executive editor and digital content manager

Wells’ missteps have surfaced a fundamental concern being echoed by executive teams in banks and other financial players:

“Does compensating for sales productivity compromise the service orientation of a financial institution?”

With over 60 years of combined experience working for and with banks and credit unions, we—Dan Kleinman and I—think the answer is a firm “no.”

That is, if everything is done properly.

Doing it right involves more than just putting together a sales plan and a payout schedule. In fact, that’s the problem with most sales programs we’ve seen in banks, particularly larger ones.

When a new initiative is thought up, a construct is created to pay retail staff for successfully meeting sales targets around that initiative. Then suddenly, banners are unfurled, trumpets blare, and it’s off to the races. This approach, besides being criminally incomplete, ignores the very fabric of a sales/service culture.

What does “sales/service culture” look like?

A “sales/service culture” is more than just words tossed around at a Senate hearing. It’s real.

Producing and maintaining one takes planning and work—actions Wells Fargo apparently did not do well.

The values in a healthy culture emphasize a blending of two approaches focused on the same result; a satisfied, loyal, and engaged customer.

The operative word is “blend.” Selling—or broadening the customer’s choices—must be balanced with service—implementing and supporting those choices.

What kind of environment does it take to achieve the right balance? One with:

• Comprehensive services offered with effective operational support systems (including sales administrative systems).

• Caring customer-focused people who have a sense of pride in their financial institution based on reputation and achievements.

• Effective management infrastructure that talks the talk and walks the walk

• A value system that places doing things “right for everyone” at the apex of the pyramid.

At the foundation of this culture are its people. People who:

• Know how to actively listen.

• Enjoy helping others.

• Work as a team.

• Accept accountability for their own behavior.

• Can communicate, and who are articulate.

Not everyone fits this description

Such people not only understand the company’s value system, they reflect it. They take pride in the achievement of the group over their own accomplishments. They get things done. And, they always have the best interests of the customer and their institution in mind.

It’s inconceivable that all 5,300 Wells Fargo staff members who were dismissed because of poor performance did not have the fundamental skills and attributes needed from the get go. Or that they could not have all been developed to effectively offer customers the bank’s services.

It’s much more conceivable that line, middle, and senior management did a lousy job selecting and training people.

Worse yet, the goal may have been to recruit aggressive, commission-oriented staff that are the antithesis of a sales/service culture. The latter may well be the case given Wells’ sales quota system.

Finding the right candidates begins with bosses

Identifying and supporting management who will train and coach the right people is the next and equally vital step.

Too often banks reward technical proficiency by placing an individual with only this skill in a management role. There is little appreciation managing others requires a completely different set of skills and attributes.

Not all senior practitioners are a good management fit. Those who lack the right skills break down the culture through counterproductive behavior.

Organizations need formalized practices reinforcing the same values up and down the management chain. The CEO has to be confident that line, branch, regional, and executive management is expressing the same sense of priority in the sales/service culture as he or she is.

Clearly, based on the public testimony given, Wells had a significant breakdown aligning their culture top to bottom.

Where does the bank meet its client?

Another key in creating a blended culture: The branch team owns the customer.

• The sales specialist helps determine the customer’s need and points the way to those services filling the void. The service specialist ensures seamless activation and maintenance of those services and problem solves any situations that may arise.

• The sales specialist checks in with the customer to make sure new needs are being addressed. The service specialist checks in to determine if quality and performance are being maintained.

Both functions want the customer to be loyal and satisfied. Both feel an ownership in the process.

Rewards aren’t just about money

Rewarding for sales and service isn’t just about pay; it’s about meaningfully reinforcing the culture.

As long as it’s genuine, sincere, and doesn’t constitute a mixed message to the staff, rewards can take many different combinations.

For example, some specialists value public recognition, individually or as a team. Others see accomplishment translated into increased opportunities (serving on committees or projects) with senior management visibility. And, of course pay is more than a symbolic gesture for work well done.

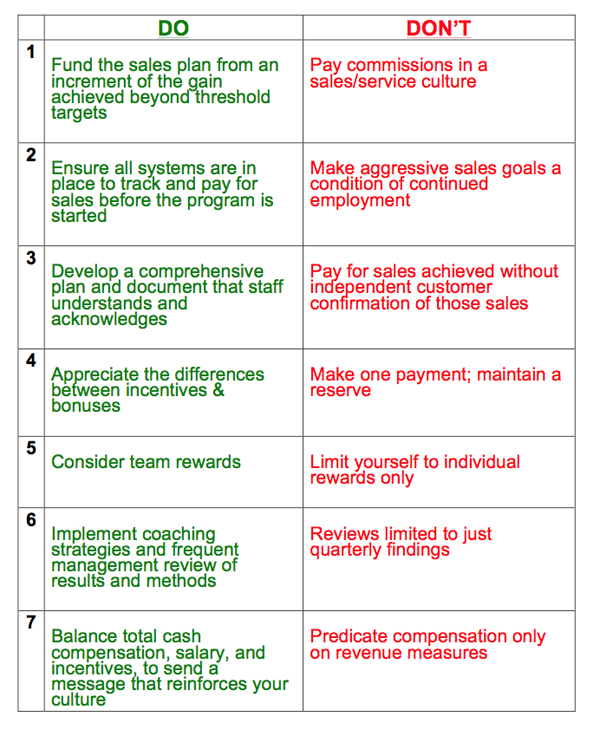

7 key points to ponder

Sales programs in a sales/service culture come with certain dos and don’ts.

Always size your sales and service staff for success, making sure you have just the right staffing for specific traffic at specific times of the day or week. This not only ensures an efficient use of staff costs but increases each specialist’s appreciation that their objectives are attainable and the environment wants them to achieve.

To stay viable in a competitive retail environment, banks have to ensure consumers are aware of all services offered. Customers need to know that someone is listening to them, tying their needs with the bank’s offerings.

That’s the nature of selling, and of serving a customer.

Coming out of the current fog and gloom

The recent cloud darkening the issue of selling services is the result of Wells Fargo’s bad practices, neglected culture, and absentee management. It is not the result of an inherently bad concept of rewarding staff who sell needed services.

This concept has to exist in a context where sales and service are seen as a team approach, where the culture influences the priority and performance of staff and management. This takes preparation and constant work. We believe the long-term rewards of increased productivity, retention, customer satisfaction, and loyalty are worth the effort.

Semper,

Mike Moebs

Moebs $ervices has a Financial Service Sales webinar on October 27: Best Practices for Successful Cross-Selling. Learn more here

Afterword

Both Dan Kleinman and I worked for Wells prior to the Norwest purchase of Wells Fargo and consulted for many years after leaving. Dan managed HR for Wells Fargo in the 1980s and for Charles Schwab in the 1990s. He is considered a national expert on the design and auditing of sales compensation plans. His book, Allstar Sales Teams, is something Wells Fargo executives and board should wish they had read long ago. —Mike

Tagged under Mergers Acquisitions, Lines of Business, Blogs, The Prairie Economist, Tokenization, Revenue, Feature, Feature3,

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients