Looking beneath FDIC's latest numbers

Strip away big bank results, and see community bank urgency

- |

- Written by ALCO Beat

The current economy, married to low-interest-rate strategies from the Federal Reserve, continues to put the squeeze on many smaller banks. And consultant George Darling expects conditions to grow worse for them yet. But he has a suggestion or two for the near-term--and some harder advice for the longer term.

The current economy, married to low-interest-rate strategies from the Federal Reserve, continues to put the squeeze on many smaller banks. And consultant George Darling expects conditions to grow worse for them yet. But he has a suggestion or two for the near-term--and some harder advice for the longer term.

By George Darling, Darling Consulting Group

If anyone glanced quickly at the FDIC Quarterly Bank Profile press release from August 28, they would get the distinct impression that things keep growing much better for the banking industry.

After all, year-over-year profits are higher. Non-performing loans and loan write-offs are lower. And loan balances are higher and the number of problem banks has fallen from 772 to 732.

However, closer review of the numbers reveals that this high level view does not capture the essence of what is happening to the majority of banks in the industry. This is especially true for banks in the community banking space.

Larger banks obscure the picture

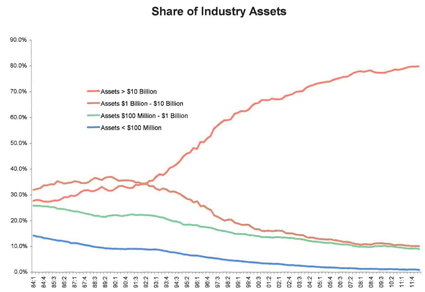

The U.S. banking industry, as a whole, is doing better. However, as of June 30, 2012, the industry now has 660 out of 7,246 financial institutions that account for 90% of all banking assets. And, the largest banks in the U.S. (over $10 billion) hold almost 80% of industry assets (see Exhibit 1). These 107 banks obscure what is happening to the rest of the industry. That prevents a clear view of the issues and challenges facing the community banking segment of the industry, unless you dig beneath the industrywide numbers.

Remaining relevant and viable as a community bank will require a re-examination of the traditional business model and the operating philosophies of the past.

True, some of the 6,586 insured financial institutions under $1 billion in assets are doing quite well in spite of the lethargic economy and high levels of unemployment. However, the majority of these banks are faced with significant challenges that could negatively impact the future viability of the community banking segment of the industry.

Those challenges are formidable.

The nation's largest banks increasing dominate the industry's numbers, which can currently skew things more positively. In spite of the top trends, smaller institutions face several key earnings challenges. (View a larger version of the chart by clicking here or on the image.)

Drilling down to community bank reality

Most community banks are faced with a plethora of pressures on their business model.

The typical community bank depends heavily on net interest income.

Net interest income (the difference between interest earned on assets and interest paid on liabilities) accounts for about 80% of total revenues for banks under $1 billion in assets. In today's economic times, loan demand from creditworthy borrowers is virtually non-existent. As a result of aggressive actions taken by the Federal Reserve to stimulate economic growth (Quantitative Easing and Operation Twist), yields on assets have been plummeting at an ever-increasing rate.

In the past, banks would simply lower the rates paid on deposits to offset the lower interest earned on assets. With current deposit rates approaching zero, many banks can no longer offset declining asset revenue by reducing rates paid on deposits. The result of these factors is an accelerating decline in the net interest income of the industry.

At the same time that net interest income is decreasing, community banks are faced with increased operating costs.

Many of these are required to comply with new regulations coming from the Dodd-Frank Act and the Consumer Financial Protection Bureau.

The combination of reduced net interest income and increasing expenses is placing the small bank business model in jeopardy. Overall, this combination threatens the viability of a large number of community banks if the current environment persists another two to three years into the future.

Finally, in addition to narrower margins and increased operating costs, community banks also need to assess the impact of the recent Basel III risk-based capital proposals. Basel III implementation, as proposed by federal regulatory agencies, would require that banks carry higher levels of equity on their balance sheets and would disallow the use of subordinated debt and trust preferred securities as capital instruments.

What can be done?

For most community banks, the downward progression of net interest income will be impossible to reverse, as long as the Federal Reserve continues to keep interest rates low.

Yields on existing loan portfolios will continue to fall as borrowers renegotiate rates and refinance existing debt. Competition for new lending relationships will place pressure on loan rates as there continues to be very little new loan demand. Investment securities offer no reasonable alternatives since the yields available will not provide enough margin to cover overhead costs that average around 3% of assets for most banks.

In an effort to slow the decrease in net interest income, banks must generate and hold loans on the balance sheet. In doing so, credit quality cannot be compromised!

On the other hand, any creditworthy borrower cannot be lost on price.

Here's one potential place to pick up some return: Rather than purchasing securities that cannot cover overhead, bankers should consider holding more of their 1-4 family residential loans instead of selling them in the secondary market. This strategy would especially include loans that fully amortize within 15 years or less.

In addition, community bankers should be aggressive in protecting existing lending relationships and developing calling programs that will enable them to "steal" good lending prospects from other banks.

The cost side must also be considered--net operating costs must be reduced.

Operating costs will also need to be reduced by most community banks. If the current economic, regulatory, and interest rate environment persists for another two to three years, banks will need to manage their net operating expenses (non-interest expense less non-interest income) to 2% of assets or less. This will require difficult decisions on closing unprofitable branches; streamlining operations; eliminating unprofitable products and services; and, ultimately, in-staff reductions. For many banks, this may also require reductions in compensation and the elimination of benefit packages that can no longer be afforded.

You can't give it away anymore

In addition to reducing operating costs, community banks that have always been reluctant to charge fees for services will need to reassess this philosophy. Levels of non-interest income are considerably higher in larger banks, as can be seen from the table below.

Non-Interest Income Trends

| Bank Asset Size |

|

Non-Interest Income Trends |

|

| > $10 billion |

1.79% | ||

| $1 - $10 billion | 1.78% | ||

| $100 million-$1 billion |

1.07% | ||

| < $100 million |

0.95% |

Community banks will need to charge for services provided--or they may no longer be around to provide that service in the future.

About the author

George Darling is CEO of Darling Consulting Group, Newburyport, Mass. Darling and the consultants of his asset-liability management firm write the bankingexchange.com "ALCO Beat" column. Darling’s professional experience includes: thirty years with his own company, two years as a senior executive with a $2 billion financial institution, two years with a Big Five Accounting firm, and ten years with IBM. He is a nationally-recognized resource for assisting financial institutions in the areas of interest rate risk management, liquidity management, and capital planning.