LCR shaking up bank deposits

SNL Report: Large-bank liquidity coverage rule changes landscape

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Nathan Stovall and Tahir Ali, SNL Financial staff writers

The liquidity coverage ratio is already changing the deposit market.

Banks' efforts to comply with the regulatory provision have changed the composition of their investment portfolios, increasing the concentration of lower-yielding securities on their balance sheets. However, the liquidity coverage ratio has also significantly increased the value of retail deposits for the nation's largest banks that are subject to the rule.

The liquidity coverage ratio, or LCR, requires covered institutions to hold "high-quality liquid-assets" greater than, or equal to, their projected cash outflows minus their inflows during a 30-calendar-day stressed scenario.

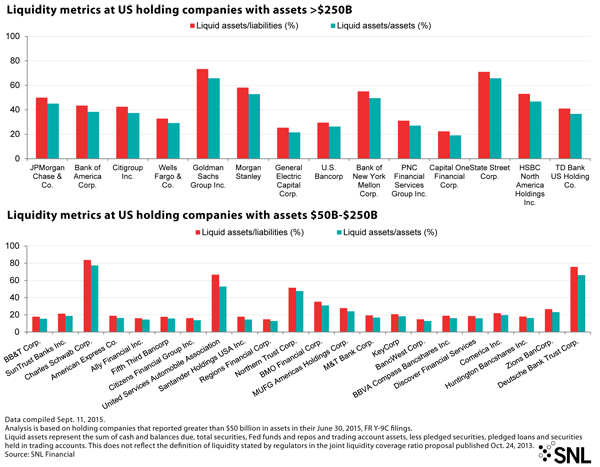

The LCR applies to banks with more than $250 billion in assets or those with at least $10 billion in foreign banking assets and subsidiaries of those large banks with at least $10 billion in assets. Those institutions began complying with the LCR at the beginning of this year and have to reach full compliance by Jan. 1, 2017.

Click to Enlarge Image

Click to Enlarge Image

Banks with assets between $50 billion and $250 billion are subject to a less-stringent LCR and will not have to begin complying with the rule until Jan. 1, 2016, though most institutions falling in that asset group have already taken steps to meet the requirement.

At banks with more than $250 billion in assets, FDIC-insured deposits are assigned a 3% outflow rate under the LCR, while noninsured deposits, including corporate deposits, receive outflow rates of 10% to 40%. Those two categories of deposits will receive outflow rates of 2.1% and of 7% to 28%, respectively, at banks subject to the less stringent LCR.

Ethan Heisler, a managing director at Citigroup, wrote in a recent newsletter for bank treasury clients that institutions, particularly the very largest banks, have worked to reduce non-LCR-friendly commercial deposits.

"The balance of excess reserves at the largest banks was consequently lower at the end of the second quarter of 2015 year-over-year, after peaking at the end of the first quarter of 2015. Consequently, retail deposits account for a larger share of the mix of deposits at the largest banks than they did a year ago," Heisler wrote in mid-August.

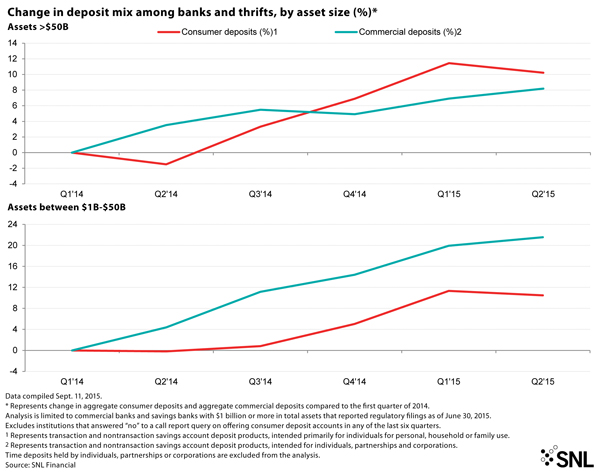

The nation's largest banks have grown commercial deposits at slower rates than their smaller counterparts. SNL data show that banks with more than $50 billion in assets have grown corporate deposits more slowly than smaller institutions, increasing those balances by 8.2% since the first quarter of 2014, when corporate and consumer data was first made available. Comparatively, banks with assets between $1 billion and $50 billion have increased those balances by 21.6% during the same period.

Banks with more than $50 billion in assets have grown their consumer deposits by 10.2% since the first quarter of 2014. Banks with assets between $1 billion and $50 billion have grown those balances by nearly 10.5% during the same period.

Some of the country's biggest banks have actively worked to reduce commercial deposits. JPMorgan Chase & Co. noted on its second-quarter earnings conference call that it has decreased nonoperating deposits across its wholesale business by $100 billion this year. The company said the decrease was partially offset by growth in consumer deposits.

JPMorgan further noted that its high-quality liquid assets had fallen $82 billion in the quarter, primarily due to lower levels of cash, but said the company remained LCR-compliant since it had shrunk deposits that receive less favorable treatment under the provision.

JPMorgan CFO Marianne Lake said on the call:

"But we are expecting retail deposits to reprice higher and faster in this cycle than in previous rising rate cycles, given the competition for good, high-quality, LCR-compliant retail deposits; given the advancements in mobile banking; given the awareness in the general environment around low rates and the desire to participate in rising rates. So when we think about our sensitivity and our reprice, we model it in assumption that it's going to be higher, somewhat higher."

A number of banks not subject to the LCR have said larger banks' reaction to the provision has resulted in them winning new commercial deposit relationships. If JPMorgan is correct, smaller banks could soon face fiercer competition for retail deposits from their larger counterparts.

Some market watchers are beginning to speculate that LCR could have another impact on smaller institutions as large banks could view them as more attractive targets in light of their strong retail deposit franchises.

BB&T Corp.'s recently announced plans to acquire National Penn Bancshares Inc. have served as fuel for this theory. BB&T, which is subject to the LCR, agreed to acquire National Penn for $1.8 billion, or a 15.4% core deposit premium.

While few observers are suggesting that large banks will embark on an acquisition spree, they do believe that the BB&T/National Penn transaction could serve as a precursor for what lies ahead and demonstrate how much value banks subject to the LCR will place on retail deposit franchises.

Click to Enlarge Image

Click to Enlarge Image

This article originally appeared on SNL Financial’s website under the title, "LCR shaking up bank deposits."

Tagged under ALCO; Mergers Acquisitions; Financial Trends; Feature; Feature3;