Building home-based wealth

Innovative mortgage design builds equity faster

- |

- Written by Melanie Scarborough

Maine's Androscoggin Bank is one of 15 institutions currently offering the Wealth Builder mortgage, invented by a pair of think tank experts.

Maine's Androscoggin Bank is one of 15 institutions currently offering the Wealth Builder mortgage, invented by a pair of think tank experts.

The history of housing finance teaches two clear lessons, says expert Edward Pinto.

First, as America learned in the downturn of 2007, the traditional 30-year mortgage is not necessarily a safe bet. Highly leveraged loans secured with very low down payments carry substantial risk of default.

Second, buying a single-family home is not a reliable way of building wealth, because properties don’t always appreciate. Indeed, Pinto’s research shows that in several major cities, such as Memphis and Detroit, a lower-priced home may gain virtually no value over decades.

Pinto is resident fellow at the American Enterprise Institute and co-director of its International Center on Housing Risk. Knowing the risks, he and a colleague have invented a potential solution that has already been introduced in the field.

Enter the Wealth Builder

The Wealth Builder Home Loan, created by Pinto and Stephen Oliner, also of AEI, “solves both those problems, which should be the goal of any housing policy,” Pinto says.

Wealth Builder consists of a 15-year fully amortizing loan that requires no mortgage insurance or down payment. Instead, borrowers pay up front for an interest rate buy-down, which allows them to build equity quickly.

In the first three years of a Wealth Builder loan, about 75% of the monthly payment goes toward principal. Compare this to a traditional 30-year loan, where about 65% would go toward interest.

Basics of how the Wealth Builder mortgage accelerates building of home equity. Click on the chart for more information.

Basics of how the Wealth Builder mortgage accelerates building of home equity. Click on the chart for more information.

“Shorter amortization builds wealth more reliably, even without appreciation,” Pinto says.

About 15 lenders nationwide now offer Wealth Builder loans. Some organizations offer the mortgages in as many as 40 states, Pinto says. Others offer them only within their bank’s own footprint.

Building consumer wealth in Maine

Among the latter is Androscoggin Bank, an $857 million-asset institution in Lewiston, Maine.

“As a community bank, we really want to invest in people within our communities and come up with new and unique ways of doing that, so we look for products that are different from what we have now,” explains President and CEO Paul Andersen. Through the bank’s work with AEI, Joe Ferris, mortgage lending manager, and Chris Logan, chief lending officer, discovered Wealth Builder Home Loan and introduced it to Androscoggin.

“There are several challenges facing people buying homes,” Andersen says. “One of those is a lack of down payment. The other is making payments work for them so they can build equity more quickly.”

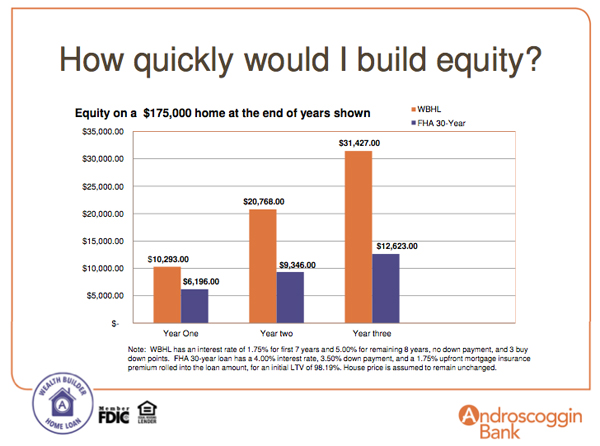

At Androscoggin Bank the Wealth Builder loan currently has a fixed rate of 1.75% for the first seven years. For years 8 through 15, the interest rate is 5%—but the loan is reset during the step-up time so the customer pays the higher interest rate, but only on the remaining loan amount.

Consequently, the higher rate isn’t accompanied by major sticker stock. Ferris points out that after 40 months of payments, a Wealth Builder Home Loan gets down to 80% loan-to-value ratio. On a 30-year loan, it takes about nine and a half years to reach that point.

“Overall, what we’re trying to do is foster people’s prosperity,” Andersen says. “This helps them pay down their principal more quickly than with other products so they build up more equity than they can otherwise.”

Andersen says that he has seen firsthand how effectively the loan works.

“My daughter bought a home last year using the Wealth Builder Home Loan,” Andersen says. “In her first year of having this loan, when she did her tax returns, she saw that $9,000 of principal had been paid down in less than a year. Someone who got a 30-year loan might have paid down $1,000 to $2,000 in that amount of time.”

Examining bank’s risk exposure

Despite the fact that they require no down payments, Wealth Builder loans are low-risk. Androscoggin requires holders to have a checking account at the bank that includes direct deposit of their paycheck and automatic transfer to their loan payment.

But the rapid acquisition of equity may offer the best security.

“The biggest risk for banks in loss of mortgages is when our clients have no equity,” Andersen explains. “If they perceive that their home has no value in a downturn, they’re more likely to walk away, leaving us to foreclose or auction. So Wealth Builder loans help the economy and mitigate our risks.”

Cross-selling opportunity for banks and brokers

One of the tangential benefits of Wealth Builder loans is that they help draw in new customers, particularly the much-prized millennials.

“It’s very hard to acquire new clients,” Andersen says. “People generally don’t change checking accounts, because of the hassle.” Yet 70% of Wealth Builder customers are new clients for Androscoggin Bank—“a very good figure,” he says.

The product also has proven easy to market, according to Marketing Director Melissa Rock, who says real estate brokers’ enthusiasm for the loans is partly responsible.

“They spurred a lot of our growth because brokers are bringing in people from everywhere,” Rock says. “This is a particular product that people really need.”

Real estate brokers number among its fans, Ferris says, because Wealth Builder loans not only finance first-time buyers, but in a very short time, those first-time buyers are in a position to buy a larger home.

“If they have equity in the one they want to vacate, it’s easier to sell because if they need to move the needle a little on the asking price, they can do that,” he explains.

The loans are proving to be good for banks, good for customers, good for business.

“Consumers love it and what you find is that, faced with an option, most are taking Wealth Builder instead of FHA,” Andersen says. “It’s giving people a vehicle to improve their lives.”

Download American Enterprise Institute fact sheet about Wealth Builder

Tagged under Lending; Residential; Lines of Business; Big Data; Feature; Feature3;