Is your liquidity plan ready for 2018?

Conditions are rapidly changing in many markets. Make sure you have a solid plan in place as you attack the New Year

- |

- Written by ALCO Beat

Regulators have some legitimate reasons to be concerned about banks' liquidity position, according to Steve Boselli of Darling Consulting Group. One example of what to think about: Is your liquidity stress testing process fresh, or has it grown stale compared to the conditions of today and tomorrow?

Regulators have some legitimate reasons to be concerned about banks' liquidity position, according to Steve Boselli of Darling Consulting Group. One example of what to think about: Is your liquidity stress testing process fresh, or has it grown stale compared to the conditions of today and tomorrow?

By Steven J. Boselli, managing director, Darling Consulting Group

On the first day of Christmas, the examiners sent to me, an MRA on contingency liquidity.

On the second day of Christmas, the examiners sent to me, a downgrade on my overall liquidity.

And on … and on … and on…

Over the past few years liquidity has been one of the largest regulatory concerns and the examiners’ focus on liquidity will remain a priority for 2018 and beyond.

In many cases, the regulatory concern is warranted.

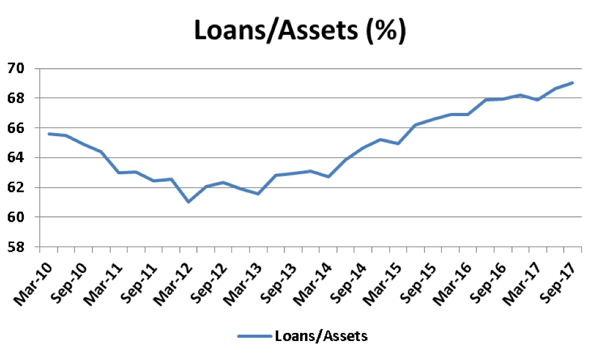

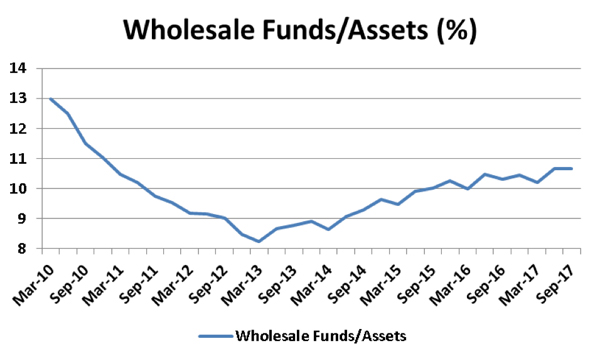

The following two charts show trends for all banks in this country south of $10 billion in assets.

From March 2012 through September 2017, loan-to-asset ratios for every community bank in this country, on average, have increased from roughly 61% to 69%. From March 2013 through September 2017, wholesale funding usage as a percentage of assets has increased from just over 8% to almost 11%.

These may not seem like material increases—especially for a single institution. However, when you look at the community banking world as a whole showing these trends, you can start to see why the regulatory concern arises.

The “30,000-foot” liquidity story is simple:

1. Slowdown on investment purchases. Given the recent flattening of market yield curves and the overall lack of slope (2/10 treasury spread is currently 57 basis points), most institutions have not been buying meaningful amounts of securities.

2. Loan growth in many markets has been strong. Loan pipelines and the overall net growth in loan portfolios across the country have been solid in most markets over the past few years. However, competition has been fierce. As a result, lenders face longer durations and tighter spreads, even as they redeploy as much lower-yielding investment cash flow as possible.

3. Distance widens between deposit and loan growth. Although deposits have been increasing, the amount of net growth has lagged the overall level of loan growth.

4. Heavier reliance on wholesale. Wholesale funding levels as a percentage of assets continue to increase. As a result, liquid asset levels continue to decline and the overall reliance on and use of non-traditional funding sources continue to increase.

The logical extension of all of this: regulatory concerns.

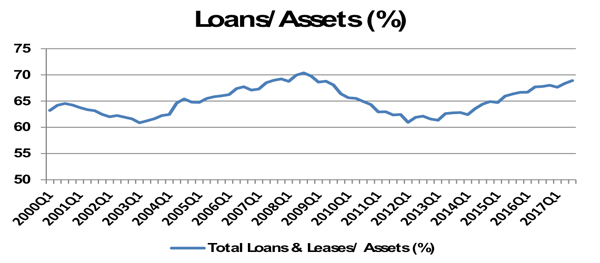

Note that if you extend the historical period of analyzing the loan-to-asset ratio for community banks, we are almost back to pre-crisis levels:

Key liquidity issues for community banks

Here are issues your ALCO should be considering:

• Liquid Asset Levels/On-Balance Sheet Liquidity.

The aforementioned reduction in liquid asset levels (cash and unencumbered bond collateral) has been a key regulatory focus in recent exams. Allocating a portion of the balance sheet to cash and fixed-income securities (vs. funding continued growth in the loan portfolio) is most likely a give-up in earnings, which can be painful on a bottom line.

Notwithstanding, recent regulatory feedback from many of our clients suggests that if you are an institution that is approaching (or already below) 10% liquid assets as a percentage of total assets, here is your warning:

Be prepared to tell your story of why you are comfortable with your current liquidity posture and how you plan to fund the growth of the balance sheet over the next 12-18 months.

• Getting a better handle on your deposit base—leveraging raw data into strategic discussions.

Many banks like to talk about this key issue. And they think they have a good handle on the recent trends in their deposit base. But when you start asking the tough questions a common answer is that additional work definitely needs to be done. In most cases, this process should have started years ago. If you do not have the tools in place to get a better handle on the strength of your core funding base, now is the time!

The following questions are commonly brought up at ALCO meetings, with uncertain and/or delayed responses:

• If you are an institution that has recently put out a deposit special to bring new money into your bank, do you have a good handle on what is actually new money vs. funds shifting from other deposit types?

• If you are indeed cannibalizing your existing low-cost funding base, where are the funds migrating from into the new premium account?

• What is the actual marginal cost of the new deposit special? What is this new product really costing you?

• Have you compared the true cost of this premium product (rate plus the cost of conversion of existing accounts) to the cost of wholesale funding?

• For the new relationships to your bank, what percentage have been cross-sold into multiple relationships?

• If these are stand-alone deposits with no cross-sell potential or have not been successfully cross-sold, does your bank look at them any differently than wholesale funding?

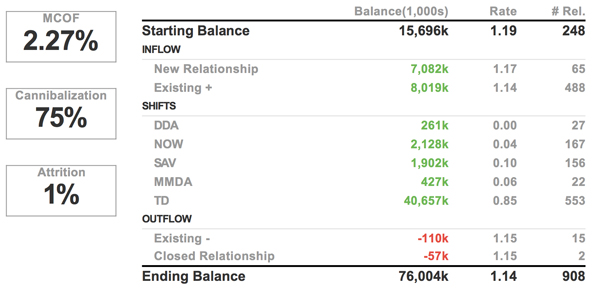

The following table isolates the true cost to one specific institution of a more aggressive deposit special. What this bank found is that although there were new account openings and some new relationships, the actual cost of this special became very expensive with the shifts and reductions in other deposit products.

Have you gone through such an exercise at your bank? Do you have the tools in place to pull together this type of analysis?

More questions that need to be answered:

• What is the plan for your largest depositors if and when they start asking for a better rate/product?

• Most banks have a plan in place for their largest 10-15 accounts. What about the top 100?

• As premium deposit specials will most likely continue to pop up in 2018, do you have an idea of what specials in your market you are willing to match?

• Do you fully understand every detail of a competitor’s special? Would you match these specials for everyone or just good core customers? How do you define a core customer?

• Are you appropriately tiered in your largest accounts?

• Does your gut say you really have a good handle on your funding base?

• Do you need to dedicate some time and resources now to elevate your overall level of comfort with your deposit base?

The potential liquidity impact and ultimate opportunity cost of not fully understanding your deposit base could be big in 2018. You need to formalize a plan on how to address these questions, sooner rather than later.

• What is your overall need for funding given your expectations for net new loans in 2018?

Many banks are at a point where much of their loan growth in 2018 needs to be funded with organic deposit growth. They may already have lower levels of liquid assets and/or a high level of wholesale funding.

This need clearly demands more of an offensive strategy to bring in new funding.

Conversely, there are many institutions that do not have a great need for additional liquidity in 2018. For them, a defensive posture to retain their best core customers may make the most sense.

The key is, even if you do not have a huge need for additional funding in 2018, meaningful deposit pricing pressures could mount as others in your local market are more offensively focused. Are you prepared to have those defensive discussions to retain your best customers at the branch level?

Consider this: The C-suite may be very comfortable having such discussions with specific customers. However, are the front-line customer service representatives at the branch level armed with the appropriate tools to have those types of discussions?

And to get down to essentials … Are you willing—and can you afford—to let some deposits walk out the door?

• The willingness of management and the board to elevate the overall level of wholesale funding.

One thing is clear, banks across this country have a very wide range in terms of their willingness to look at wholesale funding as a source of liquidity for their balance sheet.

If your bank has historically been against adding wholesale funding to your balance sheet, have you compared the true cost of funding your asset growth with retail/business/public deposits to the cost of wholesale?

If wholesale funding proves to be cheaper on paper, is everyone on the board and management team aware of the cost of saying “no” to wholesale funding? Have you quantified the potential earnings give-up?

Wholesale funding can be a very stable and reliable source of funding. Facts: You pick the term, you pick the amount, and you pick when it comes onto your balance sheet. More facts: Although it is obvious that you can never cross-sell an FHLB borrowing or brokered deposit into a good core customer with multiple relationships, you will not cannibalize a very low cost non-maturity deposit base either!

• Contingency liquidity stress testing

This should be no surprise. Having a robust stress testing plan in place has been a requirement for some time.

However, we are finding many plans that are put in place by banks are stale. And the “story” the bank is trying to tell is insufficient.

More questions:

• How often do you revisit the actual scenarios themselves?

• Do you build in growth projections based on your budget/plan?

• In your stress testing, do you cut yourself off from wholesale funding alternatives and do you have scenarios where you elevate the haircuts on your bond and/or loan collateral?

• Do you build in relief scenarios to demonstrate that you and your management team have a very good plan in place to relieve a potential liquidity stress?

• Do you document how quickly a relief scenario could materialize?

We are finding that institutions should revisit their contingency funding plan and dig into the specifics of (and more appropriately document) each of their stress scenarios.

The days of having two or three canned scenarios with no bank-specific “story” behind them is coming to an end.

A hypothetical question to pose to yourself

What if the regulators did not exist? What if banks could do whatever they wanted with respect to interest rate risk, liquidity risk, credit risk, etc.?

I asked a bank board that question the other day and everyone laughed.

But seriously, although some of the potential action items coming out of this article are designed to keep our regulatory friends happy, if the examiners did not exist, would you choose to manage these liquidity concerns differently?

Would you ignore some of the regulatory requirements?

In most cases, when you really think about it, these regulatory requests and requirements reflect tasks that you should be doing at some level, regardless. They are simply best practices.

Going into 2018, make sure you, your management team and your board look yourselves in the mirror about these key liquidity issues for 2018 and how they may or may not impact your institution.

…On the twelfth day of Christmas, the examiners sent to me, an upgrade on liquidity!

Happy Holidays! Cheers to a productive 2018.

About the author

Steve Boselli is a managing director at Darling Consulting Group, where he consults with financial institutions of all sizes across the country on balance sheet management strategies. Since joining the firm in 2005, he has held various positions within DCG, assisting clients in all aspects of ALM, including quarterly ALM modeling/consulting for advisory clients, process reviews, model validations, policy development/reviews, strategy development sessions, capital management/planning, and contingency liquidity planning. Prior to joining DCG, Steve worked for an investment firm for three years.