“I’m happy to say I’m sorry”

Part 1: Why customer problems may do more good than you know

- |

- Written by Martie Woods

What is the value of an apology?

Several years ago, when I was Chief Experience Officer at Deluxe Corp., I recall having a discussion with my team about the state of problem resolution in financial services. I remember thinking that this critical process is often such a missed opportunity. So much can be gained by doing it well.

Yet so few banks actively shape their approach.

What’s wrong with your process?

I remember my team raising good points:

• “Until banks drop the tone of superiority, no apology or resolution will feel good or sound right.”

• “What is leading banks to adopt one approach to resolution, even though customer problems vary so significantly?”

• Why do banks shy away from using humor?

Banks grow better at it

I wouldn’t go so far as to say that things have changed drastically since that discussion with my team. But I do think the industry has reason to celebrate:

1. Priority on action. Today many banks are actively working on their approach to resolution. I know this—I have worked with several.

2. Appreciating customer emotions. They are tuned into the dynamic nature of emotion and the important role it plays in dealing with problems.

3. No more superiority. For the most part, they’ve dropped the arrogance. The economic crisis helped with that.

4. And, they are actually funny. To name a few—Ally Bank, Post Bank, TD Bank, and Cap One—they (along with hundreds perhaps thousands of others) are funny, smart funny. (Catch Ally's commercials on YouTube, for example.)

However, other potential improvements have made less progress. Among these: preparing associates to handle a customer’s problem; accounting for emotion and responding with empathy; and teaching staff how to leave customers with a positive memory of the experience.

Problem experience

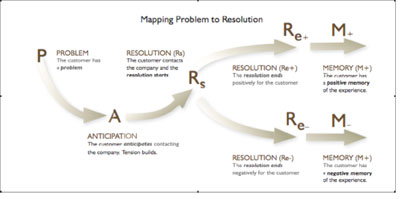

First, it helps to understand what exactly is happening in your customer’s head when they experience a problem with your bank.

Based on ethnographic research with consumers and application to several banks and credit unions, we’ve developed what we call the PARM model (Problem, Anticipation, Resolution, Memory) to better understand the problem experience:

For a larger version, click on the image.

For a larger version, click on the image.

Once a problem is discovered, your customer immediately experiences anticipation, worry, and anxiety. The extent and duration of those emotions is influenced by the severity of the problem; their history of problem resolution with your institution; and how long it takes for resolution to begin.

A key point: To customers, resolution does not begin until they speak to a live person.

So all of those online or efforts using interactive voice response systems that we designed to accelerate resolution? Fine—if they assist with information gathering and resolution overall.

But don’t fool yourself into thinking you have calmed the anxious customer who discovered an issue late last night. When your employee picks up mid-morning, they are hearing from someone who may have been fretting and stewing all night.

A (whole) ‘nother issue: your frontline employees

So, that’s a problem too, right? If resolution doesn’t begin until the customer speaks to a live person, how do we equip frontline staff to handle these kinds of issues?

Sadly, today’s situation runs more like this:

The phone rings and the service representative sighs, with exasperation.

She dreads fielding yet another call from another irate customer, regarding, no doubt, another issue she doesn’t have the wherewithal to adequately address.

The representative races through the scripted greeting.

“Good morning, and thanks for calling Our Bank,” she begins, her monotone voice matching her gloomy expression. “How may I help you?”

This same dread looms over service departments at financial institutions across the country. Our research validates what many in the industry suspected: Financial service representatives are ill equipped to deal with customers and their problems.

As a result, many of these employees develop a defeatist attitude from their inability to resolve the issues that come their way. So, in the end, we have hired a bright, enthusiastic customer-facing associate and effectively given them all reason to be less so.

The good news is that I have seen this change.

When banks give their employees access to the information they need; remove the fear of doing something wrong; and allow their own personalities to shine through, employees step up, resolve problems well, and enjoy doing so.

In our work, we received a number of stories from associates who confided in us— sharing how unhappy they were and their intent to leave the bank until we instituted these very changes. And that’s even as those changes put much more responsibility on them.

“Empowerment” is an overworked word—but it really means something.

My favorite situation was one I faced as the lead researcher on this project. After uncovering the key principles we believed would lead to strong problem resolution, we designed a pilot we would conduct in the call centers and branches of banks and credit unions throughout the country.

We taught the associates how to log each problem call, including: the issue, how they handled it, the reaction of the customer, and more. And, we followed up with calls directly to the customers to capture their perspective on the resolution experience.

None of this should have been difficult, as we had done the exact same thing earlier in our study as a baseline measure. The only difference was that we had now trained them on the new approach to handling issues, given them the okay to be themselves, and broadened their access to information that helped them diagnose and resolve problems.

Day one of our pilot I received submissions but not as many as I expected. I thought maybe they were just tired—the training would kick in.

Yet Day 2, 3, 4, 5 and on, we had the same issue. We finally reached out to find out how it was that customer problem resolution went from being a regular part of each associates’ day to being no part of their day at all. Really?

What we learned was fascinating.

Actually, these associates were solving problems, every day, every hour.

What was different was the level of competence they felt, the freedom, the strength, and, most importantly, the confidence their employer seemed to have in them.

It changed everything.

So much so that they were no longer recognizing problems as problems.

When we reached out to find out why they were no longer logging problems, they chuckled, and said:

“Funny, without all the anxiety and negativity, I forgot I had resolved a problem. I actually enjoyed my interactions because I was doing more than listening and being beaten up. I was actually resolving.”

Part 2: “Sorry, but your apology is ruining our relationship”

Tagged under Retail Banking, Compliance, Customers, Compliance Management,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story

- Economists Become More Optimistic About Credit Conditions