Alternative loan borrowers may be traditional prospects

Debt management ability found among users of payday and other short-term credit

- |

- Written by Steve Cocheo

Careful users of alternative forms of borrowing may prove to be good prospects for traditional installment credit, according to TransUnion.

Careful users of alternative forms of borrowing may prove to be good prospects for traditional installment credit, according to TransUnion.

Competition for consumer credit from inside and outside the banking business continues stronger than ever. So attempts to sift additional eligible borrowers from groups previously either evaluated—or self-selected—as not quite ready for bank credit continue. The latest example of this comes from a new study by TransUnion that indicates that some borrowers who use “alternative loans” may actually be good candidates for traditional consumer credit products.

Alternative loans typically don’t appear in traditional credit bureau files. These services include short-term debt, such as “payday loans”; point-of-sale finance offered by retailers or third-party lenders; virtual “rent-to-own” finance; and auto-title loans.

“Alternative loans are often utilized by consumers who need money fast or have no other avenues to secure a loan,” says Matt Komos, TransUnion vice-president of research and consulting. “The majority of these consumer are among the riskiest, from a traditional credit score perspective, but those who maintain satisfactory payment status on alternative loans can in fact present acceptable risks on traditional credit products.”

Release coincides with OCC announcement

TransUnion officially unveiled its research on May 24 at a meeting for banks and other users of its credit research products. However, it had been briefing reporters about the findings of its study privately in advance of that. Coincidentally, the day before the research was publicized, the Office of the Comptroller of the Currency issued new Bulletin 2018-14, encouraging banks to offer “responsible short-term, small-dollar installment loans,” which it defined as typically 2-12 months in duration with equal amortizing payments.

Comptroller Joseph Otting had spoken of his interest in getting banks back into the arena of small consumer loans earlier this year in an interview with Banking Exchange. He noted that fintech marketplace lenders had moved into such credit types because banks backed out of small-ticket consumer lending. [See related coverage of OCC’s March 23 announcement. In January the Consumer Financial Protection Bureau, now being called the Bureau of Consumer Financial Protection, announced that it was reconsidering its small-dollar lending rule, which would affect payday credit and similar lending.]

TransUnion’s Komos said that the company’s research suggests that bank lenders may be able to make traditional consumer loans to portions of the base of consumers who currently use alternative loan sources.

“This is good news for alternative lending borrowers,” says Komos, “as many of these consumers do seek opportunities to gain greater access to traditional credit products and build their credit profiles.”

TransUnion picked up a database of alternative lending borrowers in November 2017 when it acquired FactorTrust, a bureau specializing in credit reporting on such credit products. The research referred to relied on cross-analysis between the TransUnion database and the specialized records held by FactorTrust.

(“Alternative loan” refers to the types of loans, and does not necessarily involve “alternative credit,” a catchall phrase for measures of creditworthiness that have not been traditionally used by mainstream lenders that newer lenders have in some cases adopted.)

Elizabeth Pagel, vice-president, market strategy, consumer lending at TransUnion, notes that while many consumers in the FactorTrust database of alternative loan users skew subprime, nearly 40% are not subprime credits, and 12% are actually prime or above.

For some users of alternative lending products, TransUnion officials suggest in an interview with Banking Exchange, using these products may be a matter of consumers’ self-regulation.

For example, while they might know they can qualify for more traditional credit, banks for years had tended to raise the minimum borrowing amounts because very small loans weren’t profitable, due to fixed processing costs. Officials say these consumers may take a $300 payday loan to tide them over an emergency because they don’t want a $3,000 traditional installment loan. In some cases, individuals may have had trouble with traditional credit and have not yet attempted to qualify for loans with banks again.

Future performance may be better than thought

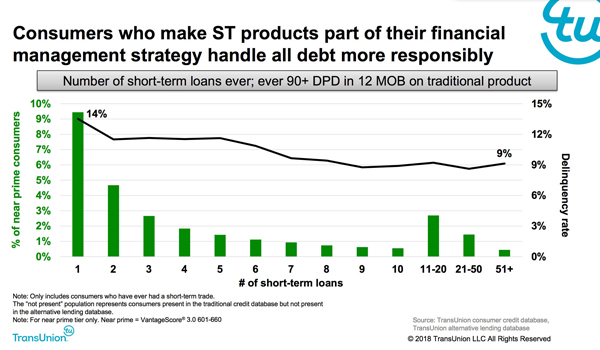

TransUnion began with a study of over 5 million consumers who opened a traditional credit product between the second quarter of 2015 and the first quarter of 2016. Researchers looked at performance one year after origination. About 8% of the sample were also present in the FactorTrust database of alternative loan users. The behavior of this subset was compared to those without alternative borrowing.

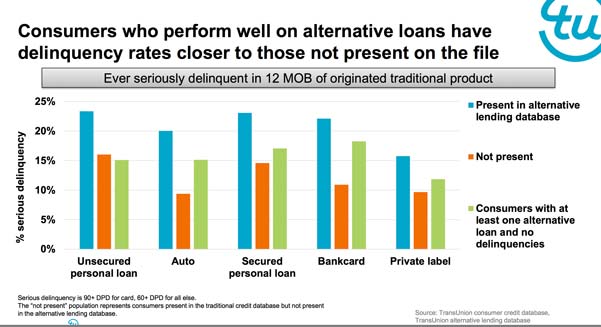

“The study corroborated that many alternative loan borrowers do present greater risks on traditional loans,” the company states. “However, there is a material subset of this population that would present reasonable risks on an auto loan or credit card, among other traditional products.”

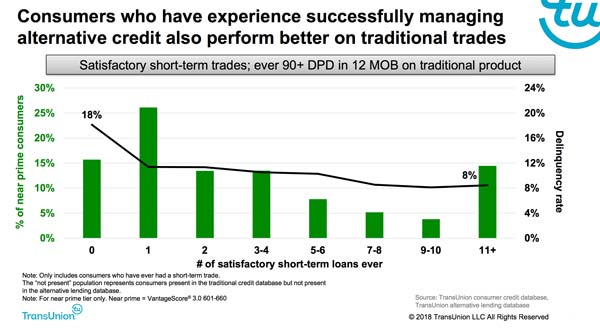

Pagel, a co-author of TransUnion’s study, characterizes the findings as a “financial inclusion” possibility. Certain metrics indicate that some borrowers who use alternative loans regularly as a financial management strategy thus demonstrate that they could handle regular payments on a larger, longer-term loan.

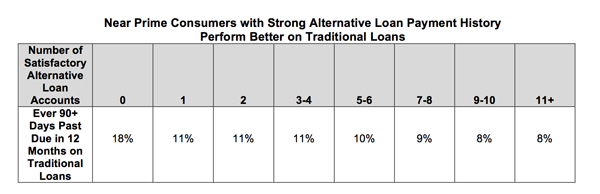

One example given by TransUnion demonstrating the general pattern concerns near-prime borrowers (those with VantageScore 3.0 credit scores of 601-660):

• About 14% of those borrowers with only one short-term loan went 90 days or more past due on a traditional account 12 months later.

• The delinquency level fell to less than 12% when a consumer possessed two alternative loans.

• The delinquency level fell to about 9% when a consumer had eight or more alternative loans over the course of seven years.

How can banks proceed?

The study notes that the findings have their limitations.

“While there are clear benefits of extending traditional credit to some alternative loan borrowers,” TransUnion states, “the study also highlighted that the majority of alternative loan consumers present greater risks than the general population. When comparing consumers with alternative loans to those without, borrowers with alternative loans are more likely to go delinquent on traditional products.”

However, the officials suggest that it is worth banks’ while to consider making traditional credit offers to these consumers. Nearly all of them have sufficient credit history to be credit scored, says Pagel. In addition, she points out, they are in the banking system already. Typically, in order to qualify for alternative lending, a borrower must have a job and a checking account.

Learn more about TransUnion’s study (Registration required)

Tagged under Consumer Credit, Retail Banking, Risk Management, Customers, Credit Risk, Feature, Feature3,

Related items

- Inflation Continues to Grow Impacting All Parts of the Economy

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples