CUs snap up business credit

SNL Report: Commercial lending by credit unions up nearly 70% in five-year period

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Chris Vanderpool and Ken McCarthy, SNL Financial staff writers

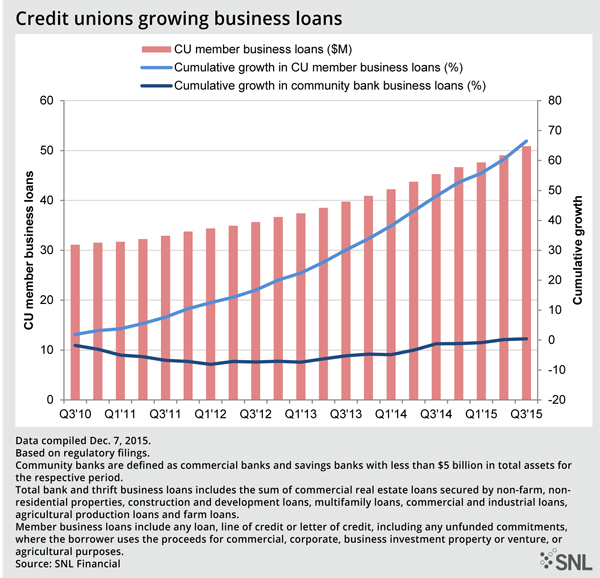

Business lending at U.S. credit unions has skyrocketed during the past five years while the nation's community banks have seen that lending line basically flatline, an SNL analysis found.

Growth in credit union business loans from the third quarter of 2010 to the third quarter of 2015 was 66.47% while commercial and savings banks of less than $5 billion in assets saw just 0.43% growth during that period. Year-over-year growth at Sept. 30, 2015, was 12.41% at credit unions but only 0.22% at community banks.

Both newcomers and experienced do it

Many credit unions that have traditionally done business lending continue to make it a core part of their strategy for 2016 and beyond. Meanwhile, some companies that have not offered those loans are now considering it, Pam Easley, president and CEO of Los Angeles-based Extensia Financial LLC, which serves as a strategic adviser to credit unions on business lending, told SNL.

Easley said the recent growth is attributable to a few factors.

First, many credit unions are seeking diversification of their lending portfolios. "A lot of credit unions have a lot of consumer-related and mortgage-related loans on their portfolios, and some credit unions have come very close to their caps for those areas," she said.

Additionally, some credit unions are finding that they can only get so much yield on Treasury activities, and incorporating a business-lending strategy can help with overall returns.

The NCUA proposed rule on member business lending has also given credit unions an opportunity to rethink member business lending and explore how they can become more involved, Easley said. Credit unions already are increasingly taking Small Business Administration-backed loans away from community banks.

How credit unions tackle the business

Nusenda Federal Credit Union has seen 19.21% year-over-year growth in member business lending. With $1.45 billion in total assets, the Albuquerque, N.M.-based credit union had total member business loans of $285.7 million in the third quarter.

Chris Clepper, senior vice-president of business services, told SNL there has been a post-recession run for credit unions in Albuquerque because some of the major community banks in the market have disappeared through consolidation, leaving fewer competitors for a growing number of loans.

He added that much of the Albuquerque economy is tied to federal spending due to the Air Force base and some national laboratories in the area.

"Historically, Albuquerque has always been kind of a lagging city economically," he said. "Usually we're a couple of years behind the national trend." So there is now some cautious optimism as the market is beginning to gain some traction with employment levels returning to previous levels. "And that's having a positive impact on business lending," he said.

The bulk of the business lending being done at Nusenda is in investment real estate, Clepper said. And as business activity has picked up in the city, the credit union has also extended its commercial real estate program to attract more owner-occupied real estate business.

Of course not all credit unions are experiencing a tremendous uptick in business lending, but slow and steady growth is fine for some.

Austin, Texas-based Amplify Federal Credit Union experienced year-over-year growth of 3.62% for business loans at Sept. 30. President and CEO Paul Trylko told SNL the credit union got into business lending "in earnest" about 10 years ago. The company looks at the offering as simply an extension of the services it provides to its members because many of them are small business owners.

"So it's kind of a natural flow for us," said Trylko.

Credit unions have a member business lending cap of 12.25% of total assets, although Senators Rand Paul and Sheldon Whitehouse introduced legislation in September that would lift the cap to 27.5% of total assets for well-capitalized companies. Amplify has about 8% of total assets now tied to business lending, Trylko said. That lending line has been steady during recent years for the credit union, as Trylko the company was able to continue lending through the recession while others were not.

He said the highest percentage of business loans for Amplify is in commercial real estate, although the credit union does some C&I lending as well. He expects to see a "nice steady growth" in business lending in coming quarters, but he said it is unlikely to grow "by leaps and bounds."

Consultant praises CUs

Extensia's Easley said credit unions were always thoughtful about risk management—even through the financial crisis—and the industry is outpacing community banks in certain areas because they are better aligned with the needs of their customers. "They know their members very well, so the credit union can assess how much risk they can take on and they can also work directly with that small business owner," she said.

Easley pointed to the Southeast as an area that has seen strong growth in credit union business lending. In addition, Austin, Dallas, and San Antonio as well as parts of southeastern Tennessee have seen a lot of activity recently. She also mentioned Chicago, and said although it is overbanked some credit unions there are doing very well in those lending lines.

Easley expects business lending opportunities to remain strong across the nation at least for the next two to three years.

Clepper said financial institutions in Albuquerque are not all going after the same markets, and because Nusenda is larger than many of the community banks in the region it finds itself more often competing with behemoths such as Wells Fargo & Co. "We actually like to work with some of the community banks to fill niches that we don't," he said.

Wells Fargo, in particular, is positioned to beat Nusenda on pricing in many deals. "So it's not that we're beating everybody out on price. I think we're competitive and I think we're in the mix, but we try to rely on our service and our community involvement to set us apart," Clepper said.

But despite the recent successes, Clepper said the outlook is mixed. From a loan-demand standpoint, the short-term future looks promising as the improving economy will drive lending. But, at the same time, some banks that have been on the lending sidelines a bit since the recession are now getting more involved. "Competition looks fierce, so it's going to be an interesting dynamic going into next year," he said.

This article originally appeared on SNL Financial’s website under the title, "Business lending soars at credit unions, small banks see stagnant growth."

Related items

- Inflation Continues to Grow Impacting All Parts of the Economy

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples