Stretching for yield

SNL Report: Some banks extending duration as reinvestment risk looms

- |

- Written by SNL Financial

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Nathan Stovall and Venkatesh Iyer, SNL Financial staff writers

The lower-for-longer rate environment has prompted some banks to extend durations in their securities portfolio to help bolster waning interest income.

As long-term rates have remained lower and even fallen further in the wake of Brexit, banks have seen their security yields, and by extension, net interest margins, come under more pressure. Some banks have kept their powder dry or invested more heavily in floating-rate bonds, hoping that increases in rates at some point will provide them relief. Others, meanwhile, are reaching further out the yield curve to mitigate persistent pressure on their net interest margins.

SNL data shows that the banking industry's security yield fell to 2.06% through the first half of 2016, down 12 basis points from 2015 and more than 20 basis points lower from 2013 as long-term rates have fallen considerably during that time frame.

The yield on the benchmark 10-year Treasury has come under pressure in the last two years and fell close to 80 basis points in the first six months of 2016 alone. The yield on the 10-year Treasury has not increased much since then. Much of the banking industry now faces reinvestment risk as they are confronted with putting existing cash flows to work at lower rates.

PNC Financial Services Group Inc. Chairman, President, and CEO William Demchak described that challenge on his company's second-quarter earnings call. PNC's security yield was 2.68% in the second quarter, but the executive noted if the company looked to replace the securities in its portfolio, new purchases likely would carry a yield of 1.69%, or roughly 100 basis points lower than the current yield on the portfolio.

"Now if we really got into an environment where we believed that we were stuck here à la Japan, which I don't think is the case, we could put liquidity to work and raise our duration of equity if we got stuck into that. So there [are] offsets to it," Demchak said on the call, according to the transcript. "Look, it is a simple statement to make that it is tougher to get to positive operating leverage without help or at least without pain from interest rates."

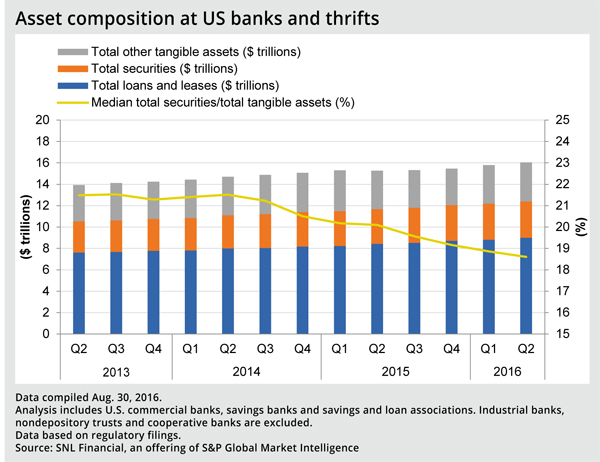

Most banks do not appear to have changed the composition of their bond portfolios that much for now. Some of the decision-making is influenced by regulation such as the liquidity coverage ratio, which requires banks with more than $50 billion in assets to maintain high-quality liquid assets greater than their projected cash outflows during a stressed scenario.

Many of those high-quality liquid assets are low-yielding securities such as Treasurys and agency debt, and banks subject to the rule held 73.1% of all securities in the industry at end of the second quarter.

Click on the image to enlarge it

Click on the image to enlarge it

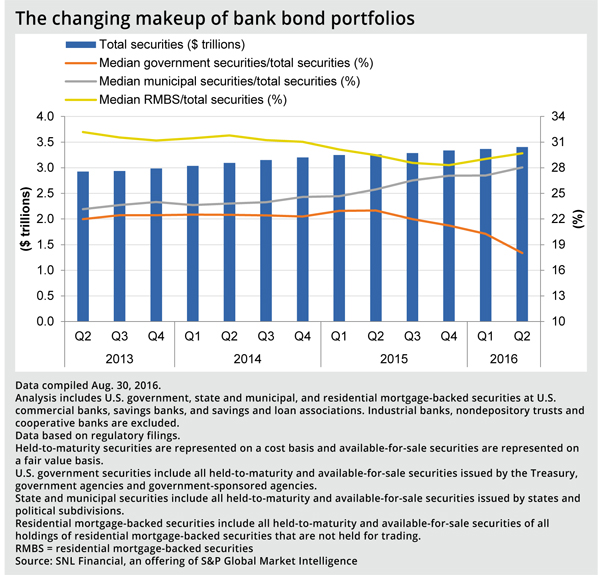

Still, the relative size of government securities—securities issued by the Treasury, government agencies and government-sponsored agencies—did decline in bank bond portfolios in the second quarter, falling to a median of 18.0% of total securities, from 20.3% in the first quarter and 23.0% a year earlier. Many of those securities are highly sensitive to change in long-term rates and likely would see their prices come under pressure if rates rise.

Even as some banks might be eying the prospect of higher rates, others are reaching further out on the yield curve to help offset the impact of the current low rate environment.

For instance, Pacific Continental Corp. said it increased the average duration of its securities portfolio to 4.2 years at June 30 from 3.7 years at March 31. Pacific Continental CFO Rick Sawyer said on the company's second-quarter earnings call that it expanded duration to generate additional interest income and yield on the portfolio.

East West Bancorp Inc. said on its second-quarter earnings call that it could entertain the same strategy as it looks to defend its current net interest margin. East West CFO Irene Oh said on the call that the duration on the company's security portfolio is "pretty low" and it would be comfortable extending from current levels.

Other bankers, however, are not changing their investment approach and say they want to be mindful of not taking on too much duration risk, even if rates remain low. Regions Financial Corp. CFO David Turner noted on his company's second-quarter earnings call that it could face reinvestment risk as the yield on the 10-year Treasury remains under pressure, but he does not believe the risk of trying to change that is worth it right now.

"We haven't extended duration. We are a little over three years right now. It's been that way for a while and we don't look to make that change," Turner said on the call.

Click on the image to enlarge it

Click on the image to enlarge it

This article originally appeared on SNL Financial’s website under the title, "Some banks extending duration as reinvestment risk looms"