Access to consumer credit grows amid concerns

Originations and balances are up—but so are delinquencies in certain segments.

- |

- Written by Melanie Scarborough

Among the trends detected by TransUnion’s latest credit research are significant changes in mortgage credit.

Among the trends detected by TransUnion’s latest credit research are significant changes in mortgage credit.

The consumer credit market performed well in Q4 2016, according to TransUnion’s latest quarterly Industry Insights.

A sampling of the trend:

• The number of consumers with access to credit products increased by 12 million, and balances rose across all products.

• Marking the highest level since Q3 2009, 80 million consumers had an auto loan or lease outstanding at the end of 2016.

• Personal loans topped $100 billion for the first time ever.

• The average mortgage balance reached a post-recession high of $194,415.

Nidhi Verma, senior director of research and consulting at TransUnion, said that the fourth quarter of 2016 showed a continued trend of steady credit growth.

“It’s one of the strongest years since the recession, as we measure originations and balance growth—and quite strong from a consumer perspective,” she said.

On the downside, delinquencies rose in auto finance and in personal loans:

• The auto delinquency rate reached 1.44% by year-end, a 13.4% increase since the end of 2015 and its highest level since 2009.

• The personal loan delinquency rate was 3.83%, up from 3.62% at Q4 2015.

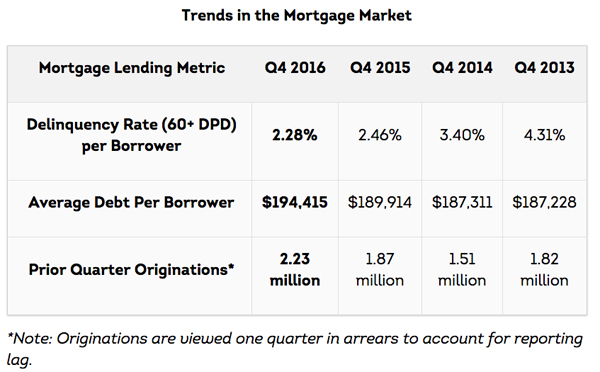

Mortgage growth up, delinquency rates down

Mortgage originations reached 2.23 million in the third quarter of 2016, the highest level in three years, and mortgage delinquencies continued to decline, as they have since 2013. They ended the year at a delinquency rate of 2.28%, which may be a natural floor.

Joe Mellman, vice-president and mortgage business leader for TransUnion, hesitates to define “normal” in the mortgage space—especially given the history of the past several years. However, he says, “We’ve been experiencing year-after-year decline in delinquencies since 2010, and we’ve flattened off at about 2.28%. Given the current lending practices, we’re hitting what could be a plateau of the rate at which rates are decreasing. We’ll need a few more quarters to solidify that trend.”

Two trends that are indisputably distinct are the growth in originations and new account balances. The size of new mortgages is at a post-recession high, which is directly linked to rising home prices.

“For the same amount of home, the borrower needs to borrow more,” Mellman says. A secondary driver could be the greater prevalence of low-down payment products than before.

“Mortgages requiring 3% down are becoming more and more available, so the average balance would be higher because there is less of a down payment,” he says.

Another factor is that the single largest driver of originations is refinancing, and interest rates remained low through Q3 2016. “What I suspect you’re going to start seeing is that interest rates have risen so re-fi has taken a hit, and that’s going to drive down origination numbers,” Mellman predicts.

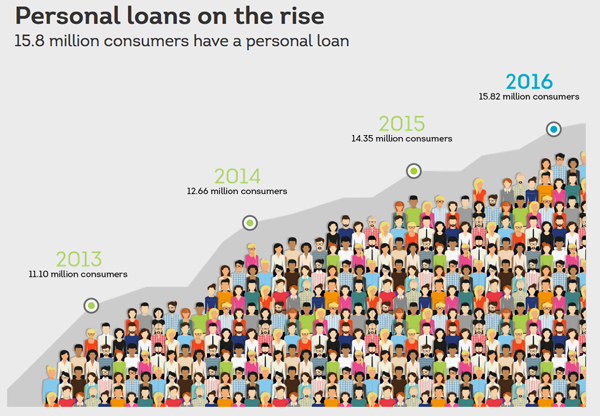

Personal loans grow in unexpected places

TransUnion found that personal loans continued to grow in both originations and balances. In Q4 2016, 15.82 million consumers had personal loans, with a total balance of $102 billion.

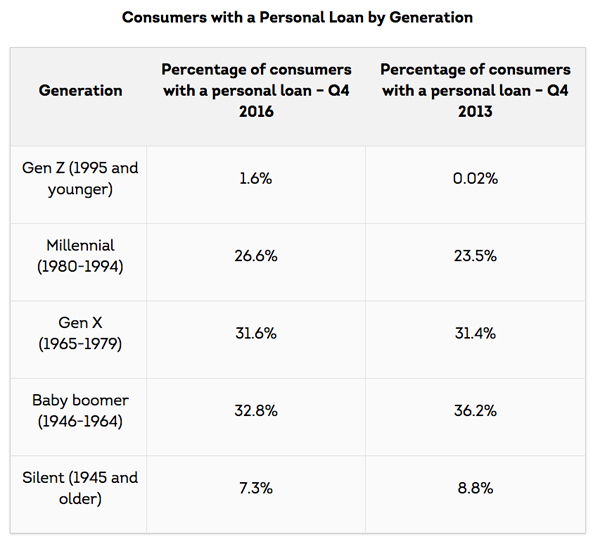

Perhaps surprisingly, more of those loans are held by baby boomers than Gen Xers or millennials.

TransUnion’s Jason Laky, senior vice-president and consumer lending business leader, says there are two principal reasons for that.

“A large use of personal loans is for debt consolidation because baby boomers tend to have a lot of credit card debt,” he explains. “The second reason is that consumers take out personal loans to meet immediate needs, such as a large repair bill that was unexpected.”

Mellman adds, “With HELOC availability being relatively low, that drives people to take out loans for home improvements.”

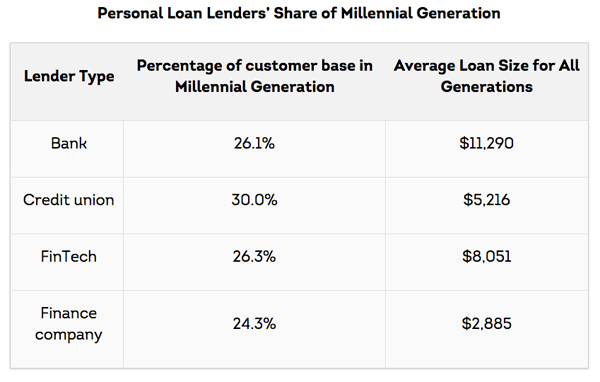

TransUnion’s study also reveals another somewhat surprising trend: Millennials turn to credit unions for personal loans more than they turn to fintech or to traditional banks. As of Q4 2016, 30% of credit unions’ personal loan customers were millennials, compared to 26% of bank and fintech customers (and 24% of finance companies’).

Consumers drive auto, credit card loans to new levels

More than 4 million additional consumers took out an auto lease or loan by the end of 2016, raising the year-end total auto loan balance to $1.11 trillion. That represents 8.3% growth during 2016, which is slower than the average 11% growth between 2013 and 2015 and reflects the slowdown in new car sales, according to Laky.

“The auto lending environment continues on a strong stable path, but certainly we’re starting to see the effects of seven years of great auto sales growth that may be finally starting to taper out,” he says. “The industry consensus seems to be that auto sales will be flat or slow growth, and financing is probably going to slow down as well.

“The other thing we’re starting to see in the trends is an increase in delinquency—17 basis points higher than before,” Laky said. That’s primarily a function of two factors, he explained: expanding opportunities into the subprime space as lenders have felt more comfortable in that market, and less dominance of new loans, as new loan growth has slowed.

According to the TransUnion research, the number of consumers with a credit card balance rose 4.4% in Q4 2016 to 139 million, the highest level since 2009, and the largest growth in credit card balances came from the subprime risk tier, where balances rose 10.8% in a year. The average card balance per consumer grew 2.8% to $5,486—up from $5,337 at year-end 2015 and the highest level since $5,609 in Q4 2010.

The credit card delinquency rate reached 1.79% in Q4 2016, an increase of 12.6% from the end of 2015, marking the highest Q4 delinquency since 2011, but still well below its peak of 2.97% in 2009.

Economic outlook differs by region

Paul Siegfried, senior vice-president and credit card business leader for TransUnion, says credit card delinquencies are particularly prevalent in states where energy production is the principal economic driver.

“Think of the loss of jobs related to oil or energy in those states—in the 200,000 range. When you see that loss of jobs, you see it on the credit cards,” Siegfried says. “We started to see that stress in the fourth quarter of 2015.”

Loss of a paycheck means paying bills with credit cards, and Siegfried said TransUnion’s data reflects that: Credit card delinquencies rose much faster and higher in energy-production states than in the rest of the nation.

For credit-card business in the rest of the country, the outlook is more promising.

“Consumer participation in cards is at an all-time high,” Siegfried says. “We’ve seen that growth driven by consumer demand and lender supply. There’s origination and balance growth—and across all risk segments. We were reporting subprime outpacing in 2014; what we’re seeing now is that growth in other risk tiers is higher than in subprime. As we see growth in outcomes, balances, and participations, we expect to see the growth of delinquencies.”

Nidhi Verma says that’s to be expected whenever there is growth into the subprime consumer space, as there has been in auto loans and credit cards. The more important point is that “we ended the year very strong in terms of credit access—and that upward trajectory [in delinquency rates] is well below where we’ve been in the past.”

Tagged under Consumer Credit; Mortgage Credit; Tokenization; Risk Management; Customers; Credit Risk; Lending; Residential; Feature; Feature3;

Related items

- Bank of England Warns AI Agents Could Need New Rules

- Why most European challenger banks fail in the US — and where the real opportunity lies

- Securitize Set for NYSE Debut Following SPAC Merger Approval

- US Banks Raise Shareholder Payouts After Passing Fed Stress Tests

- Colony Bankcorp Agrees $163m First Reliance Deal