Staying ahead of customer complaints using social media

Today no complaint should be able to grow to a major surprise

- |

- Written by Steven Ramirez

- |

Banks are facing an interesting intersection of social media and compliance.

On one hand, banks must monitor and account for social media as a customer feedback channel.

In January the Federal Financial Institutions Examination Council released a proposal, "Social Media: Consumer Compliance Risk Management Guidance." In it, FFIEC states, "a financial institution that has chosen not to use social media should still be prepared to address the potential for negative comments or complaints that arise within the many social media platforms."

In other words, you can't pretend it's not out there.

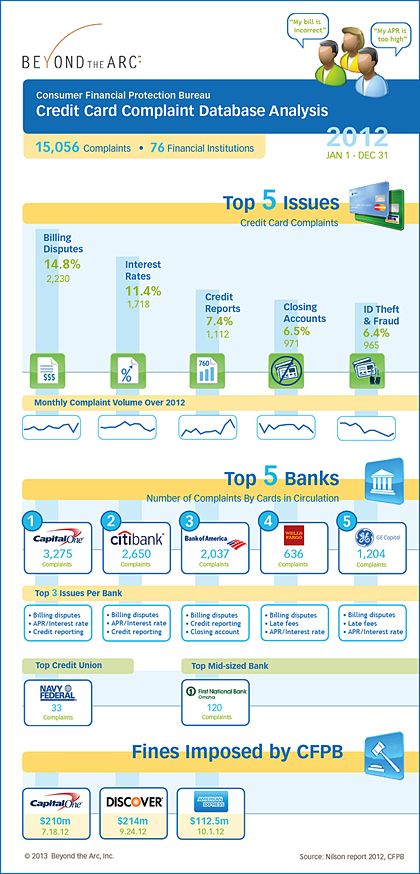

This compliance edict is also compounded by the Consumer Financial Protection Bureau (CFPB), which has been making consumer complaints related to credit cards available to the public. These complaints not only carry the potential for reputation risk, but banks have been hit with fines of more than $200 million for issues related to the complaints. With increasing regulatory challenges, financial organizations need to closely monitor customer feedback on products and services to properly address, and perhaps avert, formal complaints.

The good news: Social media provides an opportunity to get ahead of customer sentiment to address customer complaints before they are filed with the CFPB.

Top issues facing banks

The complaints in the CFPB credit card database are self-reported by consumers and are not verified by the agency. Consumers can submit complaints in a variety of ways, including web, phone, agency referral, and mail. The most frequent customer complaints for banks and credit unions generally fall into one of the following categories:

- Billing disputes

- Interest rate complaints

- Credit reporting issues

- Closing account

- ID theft and fraud

But for many consumers, complaining to the regulatory agency is not the first outlet of frustration.

Beefing on Facebook and Twitter

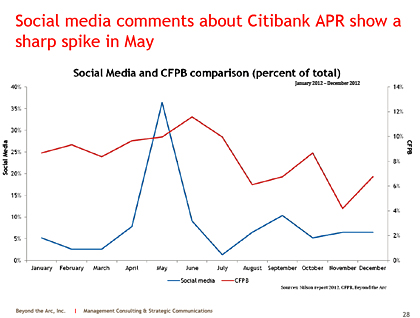

Beyond the Arc has conducted extensive analyses of consumer comments shared via social media. We identified that last year, Citibank faced a spike in CFPB complaints related to their credit card interest rates in June. Social media comments on this same topic spiked about a month earlier.

For a larger version of the chart, click on the image or click here.

And the comments are specific enough that banks can take action--a recent example:

"How's this for cynical capitalism? Rang up Citibank to pay-off and close my credit card. The lovely lady in the Philippines asked me why and I said: Your interest rate is far too high (21 percent) and she said well I'm now willing to lower your rate because you are such a valuable customer'... ‘Well, if that's the case, why didn't you drop it earlier?'

"Now that I am close to paying off almost all of my credit card debt, it feels so good to tell these credit card companies they have to drop my interest rate to something competitive ... terrible outsourced customer service"

Get in front of complaints before regulators get behind them

With viral messaging enabled by social media, negative customer experience can reach thousands of people in a matter of minutes. It is crucial that financial institutions reply quickly to customer feedback before they turn into an official report to the CFPB. The cost of not being proactive can be steep.

In September 2012, the CFPB ordered Discover to refund $200 million to customers for deceptive marketing practices. After investigating further, CFPB, in collaboration with FDIC, found that Discover misled its customers into purchasing unnecessary add-on products and services. Just as in the Citi APR case, a peak in social media comments about Discover bills preceded a spike in complaints.

Customers often try multiple times to resolve their problems. Proactively addressing regulatory risks before they result in costly fines can help banks identify key customer pain points to improve customer experience and drive retention. Whether banks choose to utilize social media to interact with customers, it is important to monitor social media to understand what customers are saying about your organization and its services.

For a larger version of the chart, click on the image or click here.

Building a VOC program

One of the best approaches to managing social media is as a part of a Voice of the Customer (VOC) program.

Voice of the Customer programs can gather data from a variety of sources and then apply text analytics. The goal is to use verbatim feedback from consumers and categorize and quantify the issues that customers raise.

Organizations can strengthen the Voice of the Customer by defining and listening to customer complaints, analyzing, and tracking customer feedback, acting to improve customer experience and measuring the results. To create an integrated view of the customer, include both internal and external measurements. Gathering data from social media about your competitors also allows you to benchmark how you're doing in the eyes of customers.

Not only can you mitigate risk through social media, but by using social media as a customer experience tool, you can strengthen customer relationships and grow your business as well.

Tagged under Compliance, Blogs, Social Media, CFPB,

Related items

- Bank of England Warns AI Agents Could Need New Rules

- US Banks Raise Shareholder Payouts After Passing Fed Stress Tests

- US Banking Regulators Step Up Scrutiny of AI Adoption

- The 'New CFPB' Era: Back to Basics Without Backsliding on Compliance

- Banking Groups Urge Regulators to Consider Stablecoin Risks