What Amazon, Google, and Uber taught customers

Part 2: Fintech lessons: Banks must balance “segment of one” thinking against “creepiness”

- |

- Written by Steve Cocheo

Are fintechs winning the race for customers? The World Retail Banking Report 2016 produced by Capgemini and Efma looks at the trends worldwide. This article presents insights from two Capgemini consultants. As companion article recaps the research.

Are fintechs winning the race for customers? The World Retail Banking Report 2016 produced by Capgemini and Efma looks at the trends worldwide. This article presents insights from two Capgemini consultants. As companion article recaps the research.

“Let’s say you are looking up 50-inch TVs on Amazon,” says Mike Leyva of Capgemini Consulting. “Of course Amazon is going to show you TVs. But guess how many other recommendations it is going to make specifically for you?”

Leyva has asked this of an interviewer, who stumbles a minute at having the tables turned: “Uh, somewhere between five and ten?”

Not even close, according to Leyva.

Amazon me, bankers

The answer is “26,” says the vice-president and head of global banking practice at the consulting firm, each buying recommendation based on what Amazon has learned about that specific customer.

What prompts this nonbanking comment is Leyva’s observation that many banks, worldwide, even those which, like a large new group in the U.K., consider themselves challengers to the status quo, don’t make use of such connective intelligence. And comparatively few venture beyond their own direct customer knowledge to learn about individuals’ needs and preferences.

For all the talk about “being digital,” that can mean almost anything, because you can digitalize almost anything, says Leyva.

He’s looking for more.

“Where is the engagement?” asks Leyva. “I’m surprised I’m not hearing more about banks wanting to create a ‘segment of one’.”

Leyva points to Poland’s mBank as an example of an institution that watches customers closely to offer products and assistance based on patterns observed, that kind of thing. Today, says Leyva, there is much more to observe, outside of a bank’s own tent.

“We don’t sit in a coffee shop and complain to our friends about low interest rates on deposits,” says Leyva. “Now we’re posting on Facebook about such things. Why aren’t more banks segmenting the customer in real time, engaging them in reaction?”

Leyva made these comments during an interview about Capgemini’s recent World Retail Banking Report 2016, unveiled in mid-April, in reaction to the question of what surprised him in the results. He’d expected to hear more about engagement. [Read a detailed recap of the study itself in “Fintech’s momentum outpacing banks.”]

Engaging versus … creepy

But there is another side of the kind of engagement that not only draws on everything a bank knows directly about its customers, but draws also on observation of social media usage and more. That side can be summed up as concerns about “creepiness.”

That is not our word, but bankers’, as quoted by Capgemini’s Bill Sullivan, the other player in this two-person interview. Sullivan, head of Global Financial Services Market Intelligence for the firm, says that he recently moderated a panel discussion about customer centricity.

“A common theme from the members of the panel was that there is a fine line between providing a personalized and customized experience based on what you know about customers,” says Sullivan, “and ‘creepiness’.”

Sullivan says banks seem to struggle with this balance. His panel members’ institutions were trying to emphasize personalization, he says, but there is a difference between delighting an Amazon shopper with a recommendation for a book they didn’t know about, and pulling information from their broader social spectrum and making financial suggestions.

In part, where there is reticence, bankers may feel there is a wall between knowing much about the customer for certain internal purposes, such as fraud prevention, and knowing much about the customer that the customers knows you know, or can guess at.

Leyva points out that four of the world’s top ten card issuers use social scoring, an antifraud method that relies a good deal on what can be learned about a prospect from social media and other internet bread crumbs. Sullivan says bankers see such services as an aid to doing a better job internally.

But the debate over personalization versus creepiness is very much of the moment. While banks wrestle with such concepts, customers seek convenience and are redefining their own feelings about such matters.

“Fintech is doing a good job of finding that balance,” says Sullivan. Customers have grown more and more comfortable seeking assistance with their financial lives outside the traditional banking arena. Ushering them into that expanded comfort zone are familiar names.

“The Googles, the Amazons, the Facebooks, the Ubers of the world are increasingly making consumers comfortable,” says Sullivan. Moreover, he says, “they are also making them more demanding, in terms of expecting ease of use, convenience, and good experience.”

Q & A on banking versus fintech

A separate article discusses the findings of the report that Capgemini put together in cooperation with Efma, the international financial services trade association. We explored the implications of fintech and other new factors in the financial environment with Sullivan and Leyva. The following is an edited summary of the conversation.

Banking Exchange: The firm’s study shows how fintech has been pulling ahead of banks, in the sense more and more consumers are using fintech and, for example, are more likely to refer a friend or family member to a fintech provider they use than a bank they use.

Was there a certain element of “perfect storm” in the way things are turning out—the crisis, an explosion of technology, and more? Would banks have been leading more of this?

Sullivan: There’s a couple of factors that have kind of created that perfect storm.

One, in general, customer expectations are rising. Two, technology is accelerating. And, yes, banks have been—I don’t want to use the word “distracted”—very focused on two things.

First is earning back customer trust and confidence. The other is the cost of doing business, notably the regulatory burden. Banks lacked the budget and bandwidth, and that left an opening for fintechs to come in.

Technology is accelerating so fast and advances are being made so fast. And access to venture capital has been quite strong recently. These factors empowered fintech to be able to start making a difference and start kind of delivering on certain pieces of the value chain. Banks haven’t quite gotten there yet.

Leyva: Remember too that fintechs also are not constrained by the bulk of being banks, right? A bank can’t just up and start a lot of these technologies, like fintechs do.

It’s a perfect storm in the sense that it’s great that all these new technologies came up. But I don’t think they’re going to disintermediate or kill banks.

Remember, there are two types of fintech firms. One kind are complete services like marketplace lenders, like OnDeck. There are also those fintechs that provide helpful services, and many banks are using their service, such as Digital Asset, Socure, IdentityMind, and ThreatMetrix.

So it’s not really a perfect storm—it’s coming along at a good time. We’ve reviewed probably close to 100 fintech services—demos, calls, had them into our innovation centers.

I think that banks are going to find a lot of value here.

Banking Exchange: Following up on the point about trust that the report discusses, I found it interesting that you had the two industries, one old and one very new. But going by the study you’ve got a highly regulated banking industry versus a comparatively unregulated fintech industry and yet the trust seems to be growing for the unregulated entities. What do you think that says?

Sullivan: Much is going on in the regulatory space and there’s a lot of conversations both in the U.S. and the E.U. about regulating fintech. The World Economic Forum came out with a study that made a pretty light recommendation in terms of what should and shouldn’t happen around fintech. [Read WEF's The Role of Financial Services in Society: Understanding the impact of technology-enabled innovation on financial stability]

Regulators are weighing whether we are at a stage where they need to start getting more involved. But they’re still trying to work through what that actually means.

And many fintechs aren’t necessarily trying to become banks. Most of them don’t want to.

Why would they want to be burdened by all this extra regulation when they can deliver some very unique specific services and capabilities to their customers—and without having to get into a lot of that hassle.

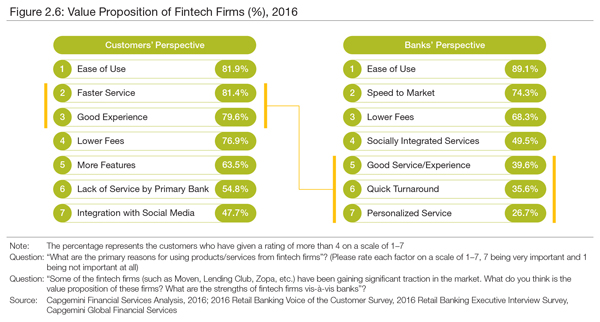

Banking Exchange: The report contrasted the value proposition of fintech firms as seen by customers and as seen by bankers. [See below.] I thought the similarities—but even moreso the differences—in viewpoint were very interesting.

[Click on the image for a larger version of the chart]

For instance, the customers ranked good experience as number three. Banks saw good experiences as number five among fintech firms’ benefits. And if you looked at the percentages the customers were almost twice as likely to refer to good experience as the banks were. Ease of use was equal by ranking and almost by percentage between both so there’s some commonality there. But there are those differences. What do you think about them?

Sullivan: Let me go back to one or two data points before I answer you.

First, we’re finally seeing customer experience level increase in banking after so many years of a kind of stagnation. However, we’re not seeing increases in profitable behaviors.

Second, only about a third of customers said they would be willing to refer their friends to the bank that they use. But when you look at fintechs that number jumps up to 55%.

So fintechs are actually really doing a better job and they’re gaining more referral mindshare than banks are. And I think that’s what leads into the chart you’re referring to.

Banks realize the ease of use the fintechs are providing is better and it’s a differentiator for them. But you’re right the fact that you have faster service and good experience is pretty close to the ease of use on the customer side of the chart. But only about 40% of the banks actually felt that fintechs had a differentiated offering when it came to good experience and only about 36% when it came to quick turnaround.

That’s really telling. Banks need to be thinking about what’s wowing customers that is helping to earn that referral mindshare. Because that’s going to be a critical piece moving forward. It may drive more and more investments by banks in fintech and more collaborations between fintechs and banks.

Banking Exchange: Mike, going back to your point about Amazon. Personalized service is in last place of what’s showing in the rankings here for banks’ perspective—only 26%.

Leyva: That shocked me. I know of a bank that really gets it. Unfortunately I can’t open an account there—I wish they’d let me—it’s USAA. Their customer experience is noteworthy. For example, they offer voice banking—they have a very comprehensive system powered by Nuance so you can say “Transfer $500 to my wife,” and it happens. USAA has also been doing face recognition for a while.

They really have it “experienced out” and a very high satisfaction rate. But I’m disappointed in banks in general.

Banking Exchange: The report discusses the need for banks and fintech firms to work together, leverage each other’s strength. Does the difference in ownership structure play into fintech being absorbed over time into the traditional banking business? Much of the investment in fintech resembles private equity more than it does the banking type investor which tends to have a somewhat longer-term outlook.

Leyva: The only ones I see being acquired by banks are those that perform a specific function like peer-to-peer payments. But fraud management, that kind of service, I can’t see why a bank would buy that, though they would use it. Most fintech firm are just technology providers.

Sullivan: Only about 18% of the banks that we talked to said that acquiring fintech was a core strategy that they were looking at in terms of building capabilities. It is more of a collaboration, a partnership opportunity. Almost every bank we contacted is having conversations.

And a large percentage of the fintechs that exist today won’t be around in a year or two, not because they got bought up but just because didn’t have a viable business model or they simply didn’t have the funding or they weren’t solving a problem. And there will be some incredibly successful ones.

Banks are trying to cut through the noise and identify where the valuable ones are, who to try to partner, leveraging the strengths of the bank and the fintech firm for a symbiotic relationship.

Tagged under Management, Lines of Business, Retail Banking, Customers, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story