6 ways to sharpen social media skills

Social’s here to stay. Fitting it into your bank’s strategy requires a measured approach

- |

- Written by Lisa Joyce

- |

It’s showtime for social media for banks. The numbers are staggering and bank involvement is growing. A key piece of advice from the experienced: People engage in social media to address a fundamental human need—to matter. So be genuine and talk to people online.

It’s showtime for social media for banks. The numbers are staggering and bank involvement is growing. A key piece of advice from the experienced: People engage in social media to address a fundamental human need—to matter. So be genuine and talk to people online.

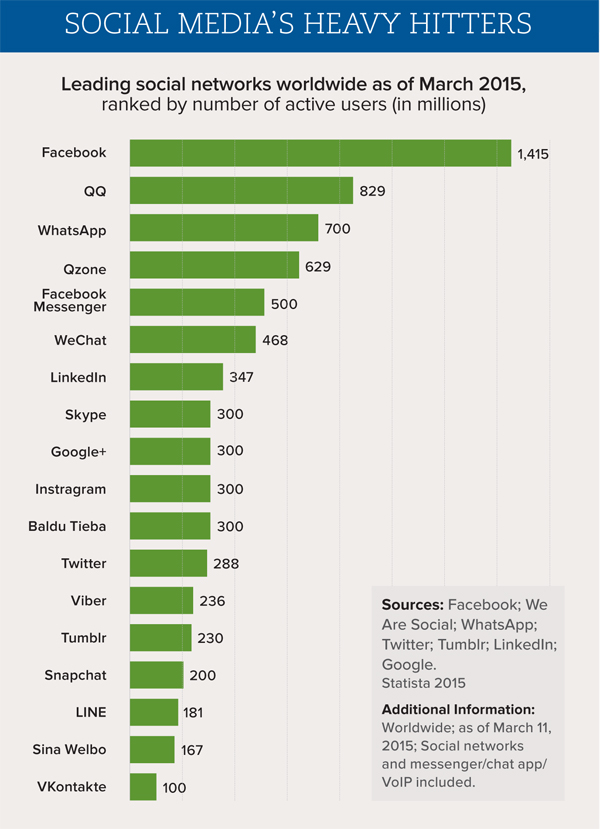

For sheer magnitude, social media usage is staggering. That would be true even if there were only Facebook, which has 1.4 billion active users. But the accompanying chart from Statista shows the wide range of social media services globally, including China-based Tencent QQ and Qzone with 829 million and 629 million users, respectively; LinkedIn with 347 million active users; Google+ and Instagram both with 300 million; and Twitter with 288 million.

Clearly, social media is not a passing fad. Those numbers are both daunting and an indication of the potential opportunity for companies that can successfully navigate social media’s continually churning waters.

Despite being a highly regulated and, by nature, conservative industry, banking is already broadly involved in social media: 83% of financial institutions have a social media presence, according to September 2014 research from the Bank Administration Institute (BAI Retail Banking Outlook: Banker Perspectives on the Financial Services Industry). That figure, however, covers involvement ranging from active to dipping in their toes. The research also found that the most often used social media platform is Facebook (67%), followed by Twitter (24%), LinkedIn (4%), and “other” (4%), including Pinterest and Google+.

But even the 17% of banks that say they don’t have a social media presence are still participating in social media, argues Eric Cook, digital strategist with WSI and cofounder of DigitalRCP, a firm that helps businesses manage digital risk. Cook tells of a $2 billion bank that did not have an active social media presence—or so it thought—until it discovered 21 unauthorized Facebook pages with the bank’s name—some with not-so-favorable reviews. (A quick search on Facebook for “I Hate Bank of America” reveals dozens of unauthorized pages.)

“You may be active or you may be passive, but you are still involved in social media, whether you like it or not,” says Cook.

If you’re going to participate in social media—whether by choice or by force—it makes sense to create an overall social media strategy. But the pressure to just jump in and start posting on Facebook can be overwhelming, putting banks in the position of throwing spaghetti on the wall and seeing what sticks, rather than crafting a well-thought-out strategy, says Ron Shevlin, director of research for Cornerstone Advisors, Inc.

Instead, Shevlin recommends not getting caught up in the competitive whirlwind and taking a measured approach to social media. “You’ll read plenty of articles that warn you of getting left behind, but you won’t. This is no time to try to keep up with the Jones.”

A measured approach doesn’t mean no approach, so it’s a good time to ensure your social media strategy is in place. The strategy should encompass more than how often the bank plans to tweet or how often it will update its Facebook page, or even which platforms to participate on. The strategy includes how the bank will measure the impact of social media, how it will structure the organization to best leverage social media, and what it hopes to accomplish.

The following is food for thought as you start to define and refine your social media strategy.

Shhhhh. Listen

In social media, sometimes silence can be golden. Banks are often overwhelmed by the thought of constant tweets, YouTube videos, and Facebook postings, but there is an advantage to simply sitting back and listening, notes Chris Lorence, executive vice-president and chief marketing officer for the Independent Community Bankers Association. “There is no rule that says you have to start posting,” says Lorence. “Open a social media account and monitor what is being said about your bank and your competitors.” Of course, the sheer volume of content on social media can be difficult to consume, so banks will need to consider how often and what they will listen to.

Listening also will help you create a social media strategy that will allow you to post relevant content, says Cook, adding that there is a misconception that banks have to post content. Instead, he says, listen and if someone asks a question or poses comment and you can offer help or information, respond. Otherwise, just listen and learn.

Pay attention to customer service

The number one reason banks maintain a social media presence is to address customer service questions (see “Top 5 Reasons Financial Institutions Maintain a Social Presence,” opposite). However, few industries have done a good job of using social media for customer service, according to Robert Harles, managing director and global lead, social media and collaboration, for Accenture.

Part of the reason is response time. The average bank response time, according to the Sprout Social Index (December 2013) is ten hours. But there are a few banks that respond more quickly. For example, TD Bank’s average response time of 75 minutes is much faster than the response time at other banks, according to Engagement Labs.

Indeed, customer service remains a vital component of TD Bank’s social media strategy. Vinoo Vijay, chief marketing officer, says the bank entered social media in 2007 with a Facebook page for college students, but that the bank’s social media initiatives gained steam when it began using social media to answer customer questions. Today, the bank’s 70-member social customer service team fields questions from a variety of social media platforms.

Although the bank’s social media strategy is grounded in customer service, TD Bank has expanded beyond answering inquires. The bank employs a heavy localization strategy for its frequent posts and tweets, and often uses viral videos to extend the brand. A recently launched viral campaign #TDThanksYou highlights TD Bank employees surprising customers with special thank you messages. The campaign, designed to pull at heartstrings, also encourages customers to share their own life memories at #TDThanksYou.

Handling the negative

Negative comments are par for the course on social media, and banks need to include a policy for responding to them as part of their social media strategy.

When confronted with a negative comment, the best approach, often, is to acknowledge the problem and state how you will address it, says Cook. Remember that your response isn’t just for the person who posted the negative comment, but for anyone who reads the post. Even if you decide to pick up the phone and call the customer, ask that person to post the resolution on the social media platform, advises Cook. Otherwise, it will look like you ignored the situation.

Another—although not failsafe—way to determine whether or not to respond to negative comments is to look at the commenter’s “social power,” says Cook. If a negative review is posted by a Twitter user with ten followers, you may decide not to respond. If the commenter has thousands of followers, you may want to reconsider. However, Cook reiterates that you need a risk mitigation policy in place to drive that decision-making.

Don’t be socially “landlocked”

Debbie Bianucci, president and CEO of BAI, notes that financial institutions are experimenting with the right organizational structure to support social media. Just over half (51%) of respondents to the Retail Banking Outlook survey have an individual or team who spends a significant amount of time on social media.

There is no right or wrong way to organize social media. Connecticut-based regional Webster Bank ($23 billion in assets) has experimented with several organizational models, reports Michael Bernard, vice-president of internet banking, but, today, has a dedicated social media team that includes marketing and customer service.

It is important to recognize that a bank’s organizational structure has an impact on the success of social media, according to Accenture’s Harles. Many banks have built what he calls “landlocked” social media teams, which make it difficult to measure the strategic impact of social media across the enterprise. Instead, Harles recommends that banks build a “social enterprise” that infuses social media across the banking organization.

From selling to engagement

According to the Accenture 2014 North America Consumer Digital Banking Survey, 22% of millennials look for financial service advice via social media, yet nearly three-quarters (71%) consider their banking relationship as transactional rather than being driven by advice or a broader relationship.

“Pitching mortgage rates is not very relationship-driven,” says Cook.

Moving from product promotion to effective content marketing is a challenge for all industries, says BAI’s Bianucci. What makes this transformation tricky for banks, however, is that they must balance the fluid nature of social media with a highly regulated environment.

Another challenge: Marketers are used to communicating with prospects and customers in a certain way, and traditional marketing does not translate well to social media, explains Cornerstone Advisors’ Shevlin, adding, “It sounds easy to communicate differently, but it isn’t.”

Shevlin, a frequent Twitter user with a substantial following, often tweets about banking, but he also tweets about nonbanking-related topics (steering clear of controversial topics, such as religion and politics). “You can’t always be serious. Look to give a different or entertaining perspective that allows you to just interact with your customers,” he suggests.

There are examples of banks getting engagement right. FirstBank Holding Co., Lakewood, Colo., has been using social media for several years, initially starting with Facebook and expanding into other social media channels as they became more popular, notes Brian Jensen, senior vice-president. In addition to Facebook, the $15 billion-assets bank has a presence on Twitter, YouTube, Google+, Instagram, and LinkedIn, and hosts a company blog.

The bank tries to engage customers with unique promotions and content that customers will share with their family and friends. “Our goal is to provide interesting content that supports the bank’s brand in a fun and approachable way,” says Jensen.

FirstBank used social media as well as its website to spread the word about its Capture the Cube competition that challenges visitors to find orange cubes hidden at Copper Mountain ski resort, which can be turned in for a free snowboard or pair of skis. The bank encourages the winners to “Brag to your friends and revel in their jealousy.”

FirstBank also has leveraged Twitter to provide race coverage of the USA Pro Challenge professional cycling race in Colorado as well as related interviews with cycling experts.

Not just metrics, the right metrics

So how do you measure the return on investment on social media? Rather than getting caught up in metrics, such as number of re-tweets or likes, banks need to step back and ensure that their social media activity is tied to definable and discrete business objectives, says Shevlin. “Many banks look at what they are doing on the individual platforms instead of what they are trying to accomplish. Stay grounded with business objectives and goals,” he says.

The economics of social media differ from traditional marketing as well. “Every outbound communication with prospects and customers has a high price tag. Social media costs next to nothing, so the danger becomes sending out too much information. Banks need to ask themselves if there is an optimal number of messages you can send out before having a negative impact, says Shevlin.

Harles agrees, saying bankers need to apply business 101 to social media. Unfortunately, most don’t apply the same rigorous lens to social media as they do other bank initiatives. “Right now, bankers are worried about being a good practitioner,” says Harles. “But senior executives are beginning to ask how social media is driving strategic impact.”

Webster Bank has key metrics to measure the value of social media. For example, the bank measures the beginning “customer sentiment” of each service opportunity it captures, and aims to improve that sentiment by the end of the interaction, says Bernard. The bank also employs monitoring tools that provide overall community size and engagement level data that the bank uses to measure social campaign outcomes.

TD Bank’s metrics vary based on the social media activity, notes Vijay. The bank tried to implement a single metric across all social media interaction but found that they weren’t getting a complete picture of social media’s impact. “You can’t look at social media through a narrow lens,” warns Vijay. “Social media touches every part of your business. It is not about measuring a win/lose, but about gaining a deeper sense of who your customers really are and how to best engage with them.”

Banks also can make the mistake of getting caught up in analytic tools touted by vendors. Shevlin attended a vendor presentation about a tool that allows banks to uncover clues in tweets that a consumer is thinking of buying a house. Shevlin’s pointed response: “What percent of Twitter users are tweeting clues that they are in the market for a mortgage? Why would you waste your time trying to find these two people? You have more important things to allocate your resources to.”

The wrap

“Social media is an exciting opportunity for making connections,” says ICBA’s Lorence. Vijay adds that, by its nature, social media requires letting go. “Don’t worry about the perfect response. Let the experience be more human.”

Be human, but take a strategic approach. Harles notes that taking a measured approach to social media is a good thing, since those banks tend to think about the strategic impact they want to drive. He adds that the reason people engage in social media is to address the fundamental human need to matter. “Be genuine and talk to people. If you keep that as the North Star, you can’t go too far wrong.”

Tagged under Mergers Acquisitions, Blogs, Social Media, Feature, Feature3,

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients